Lecture 1

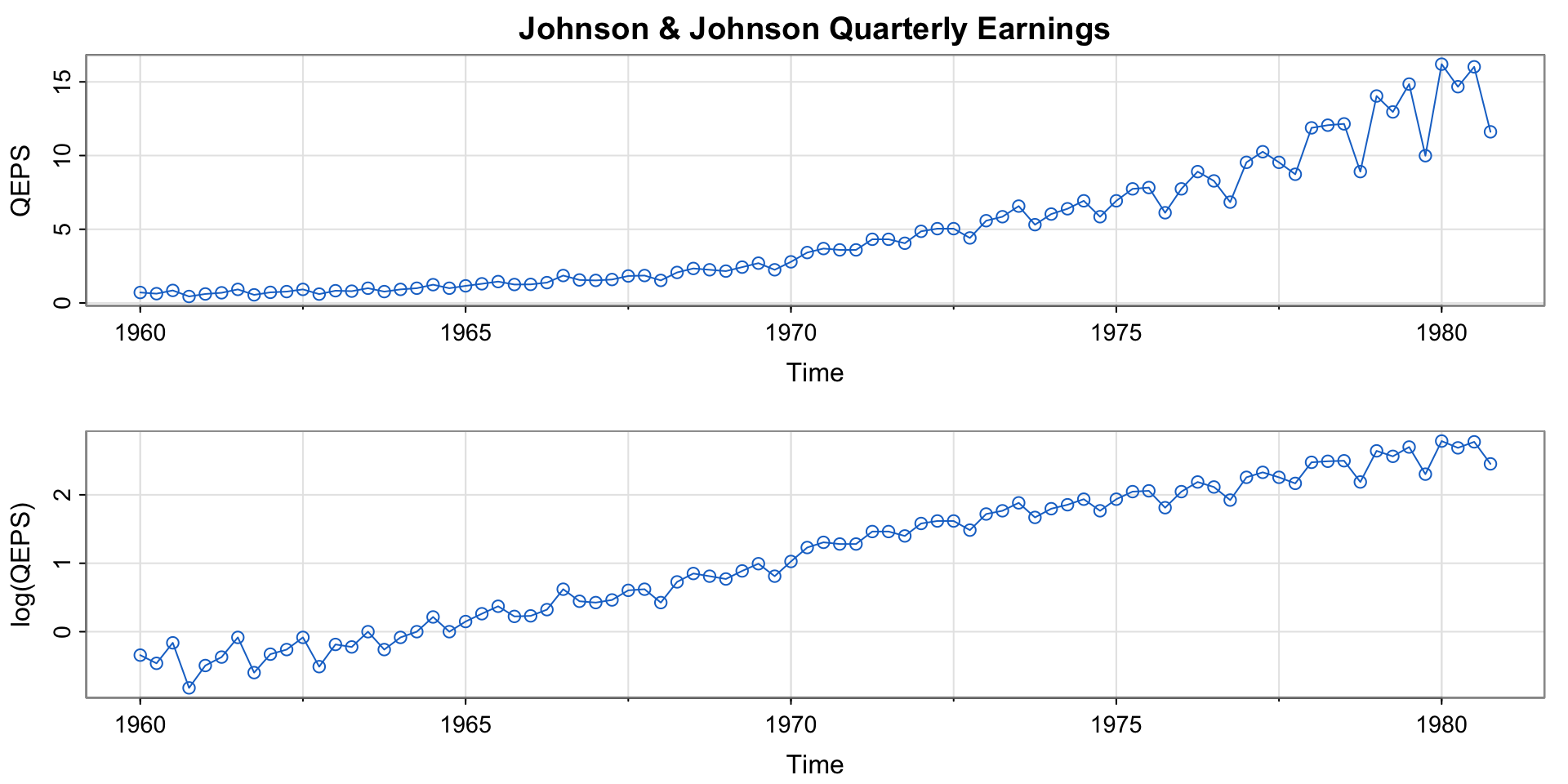

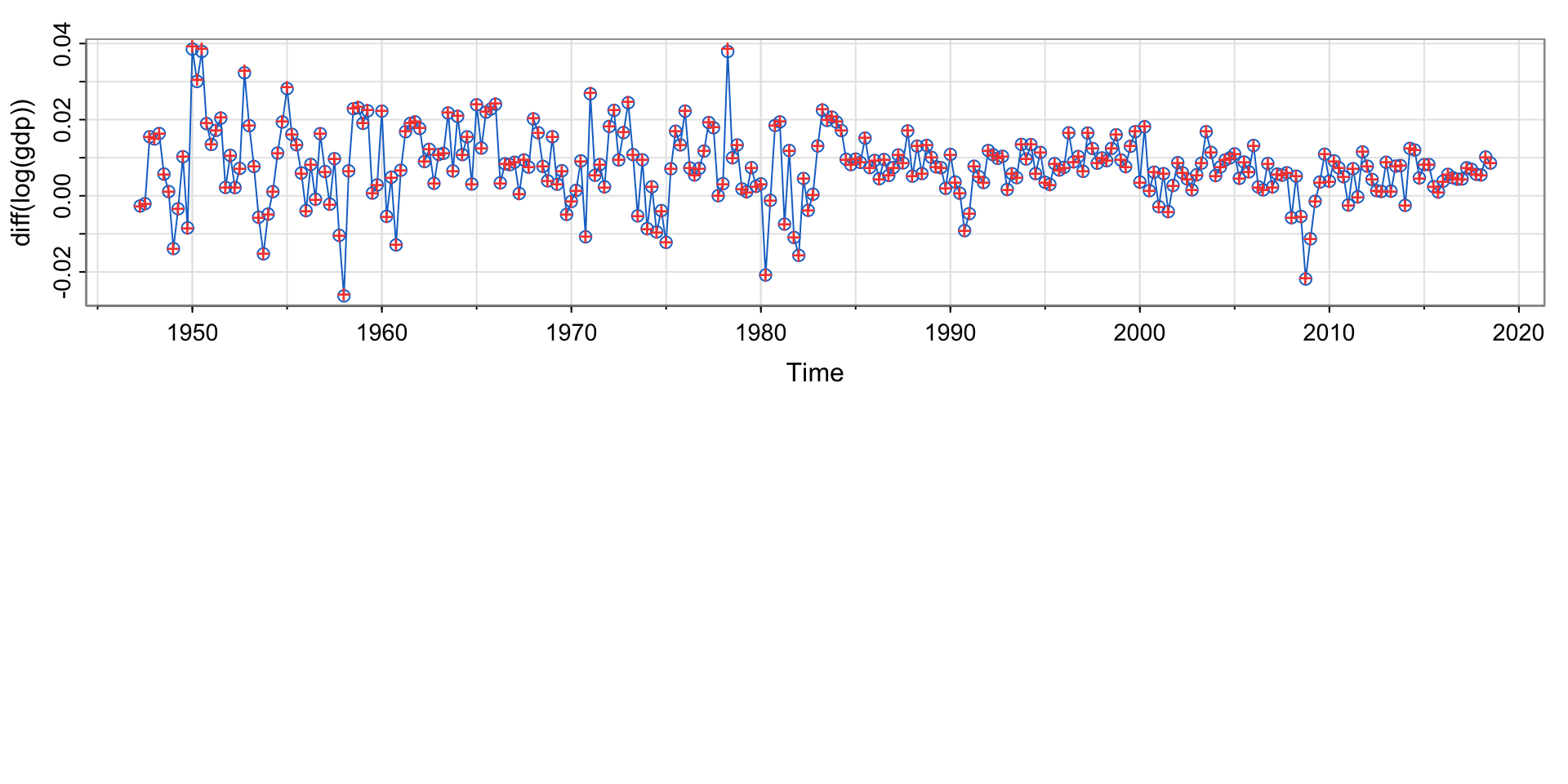

Example 1.1 (Quarterly Earnings)

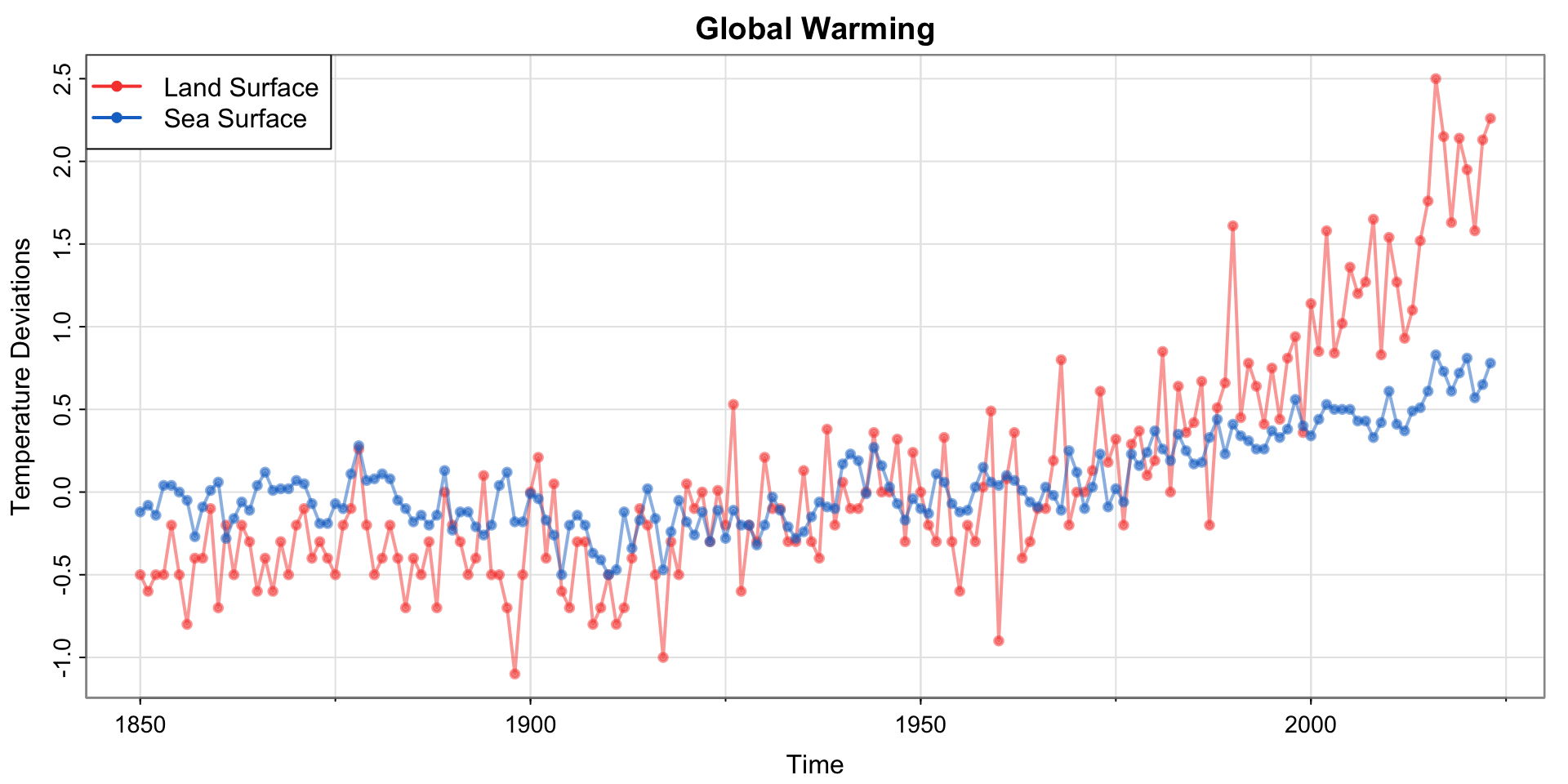

Example 1.2 (Climate Change)

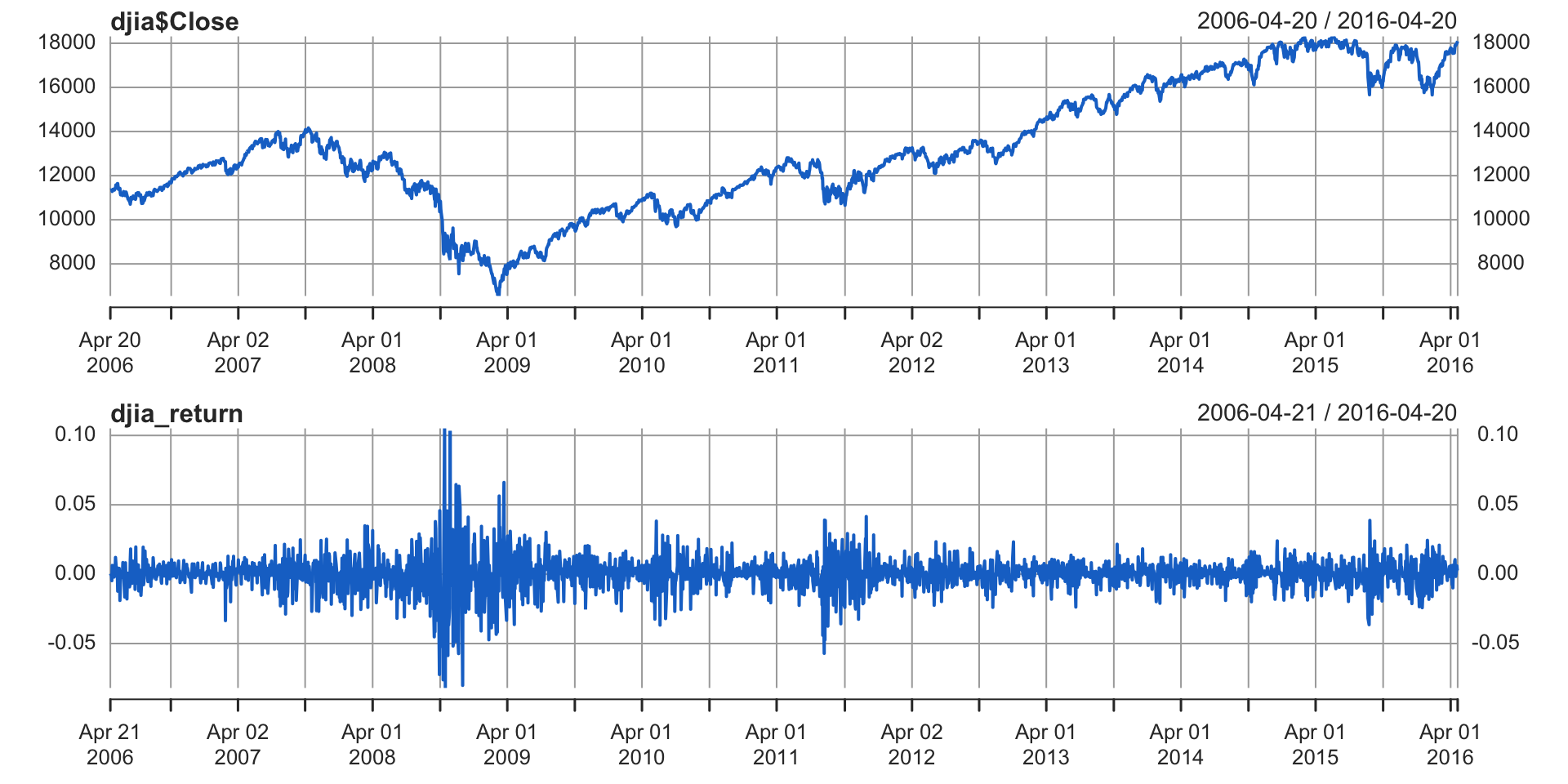

Example 1.3 (Dow Jones Industrial Average)

Code

Code

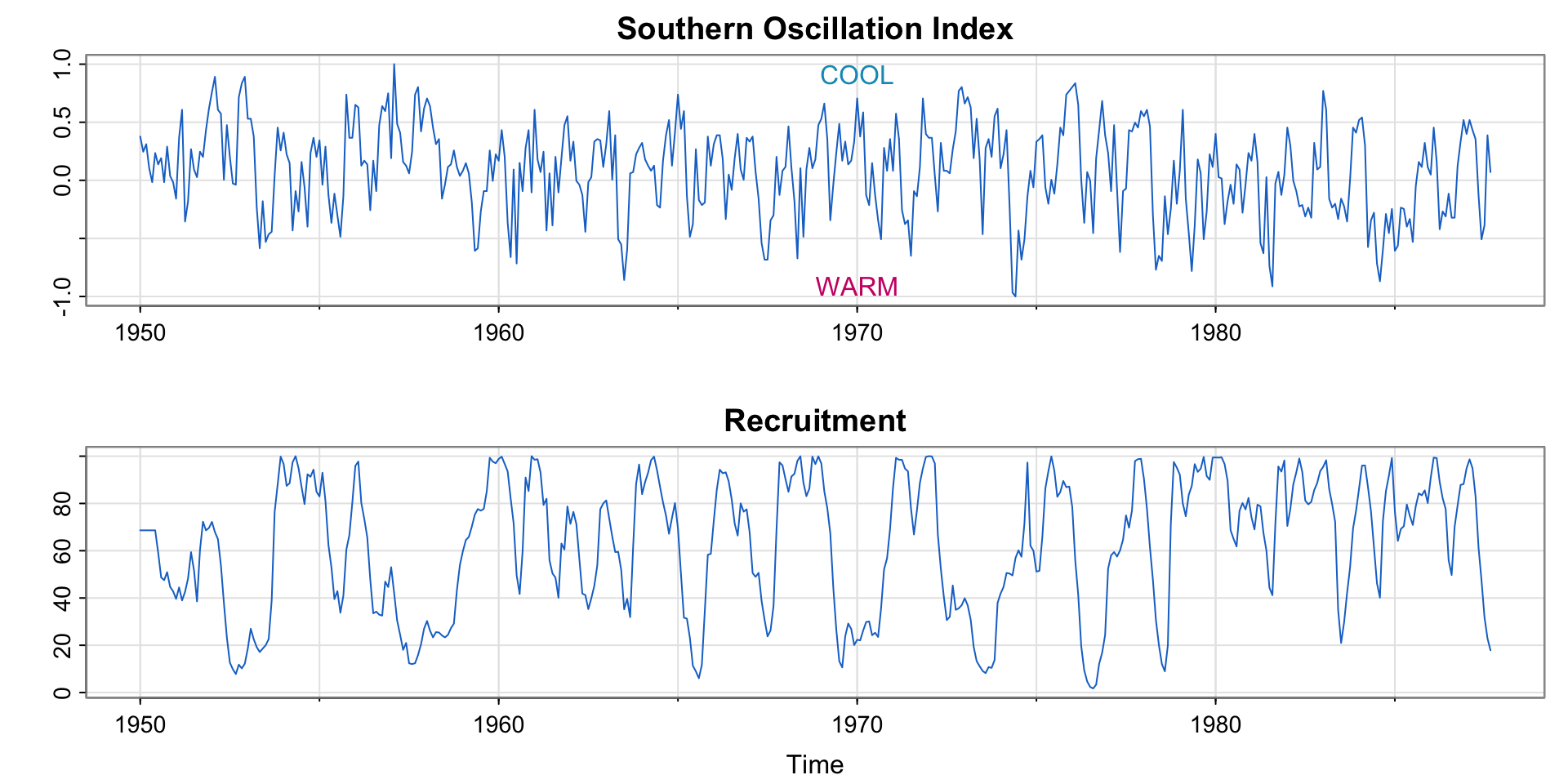

Example 1.4 El Niño

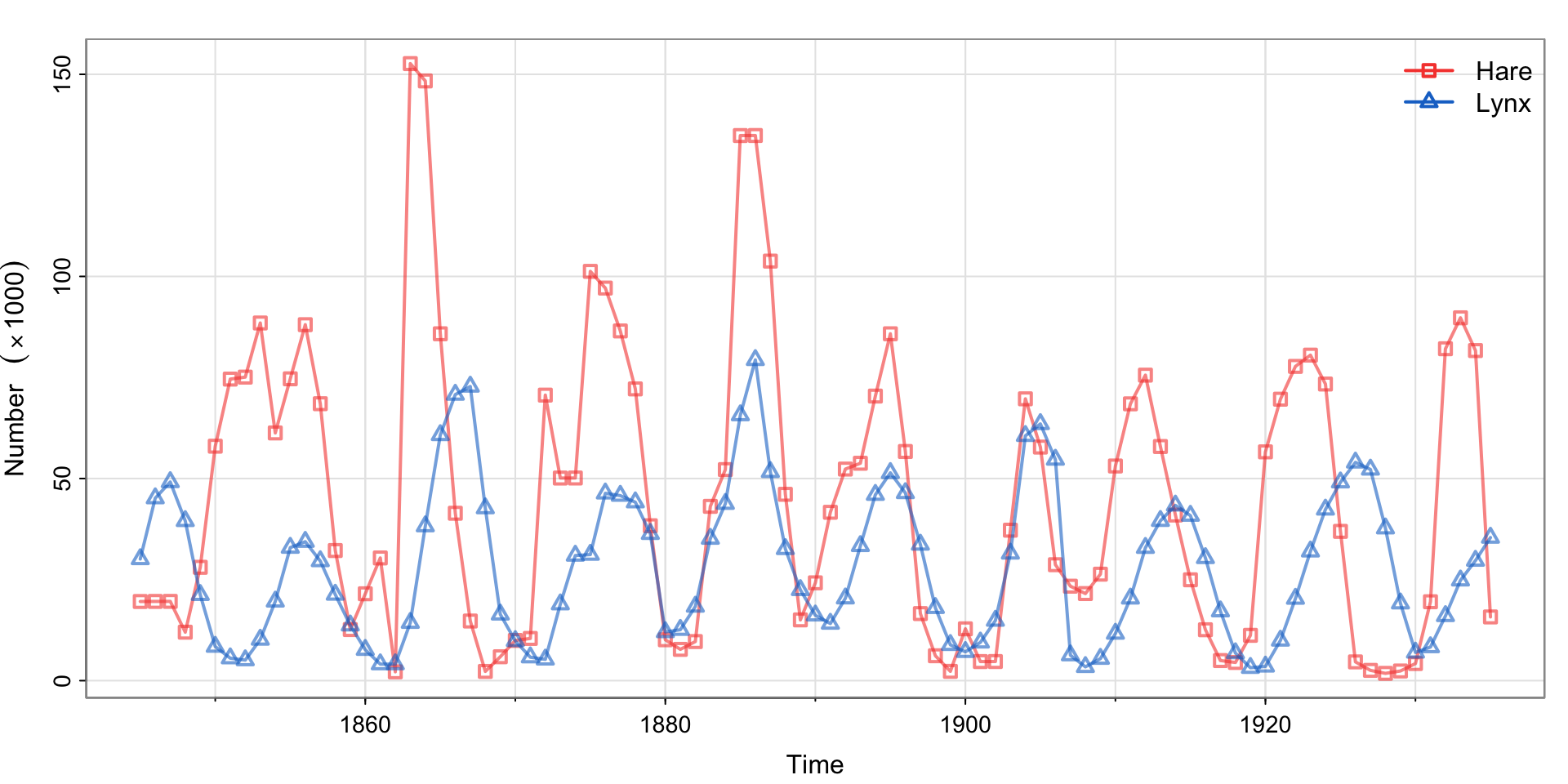

Example 1.5 (Predator-Prey Interactions)

Cute animal pictures

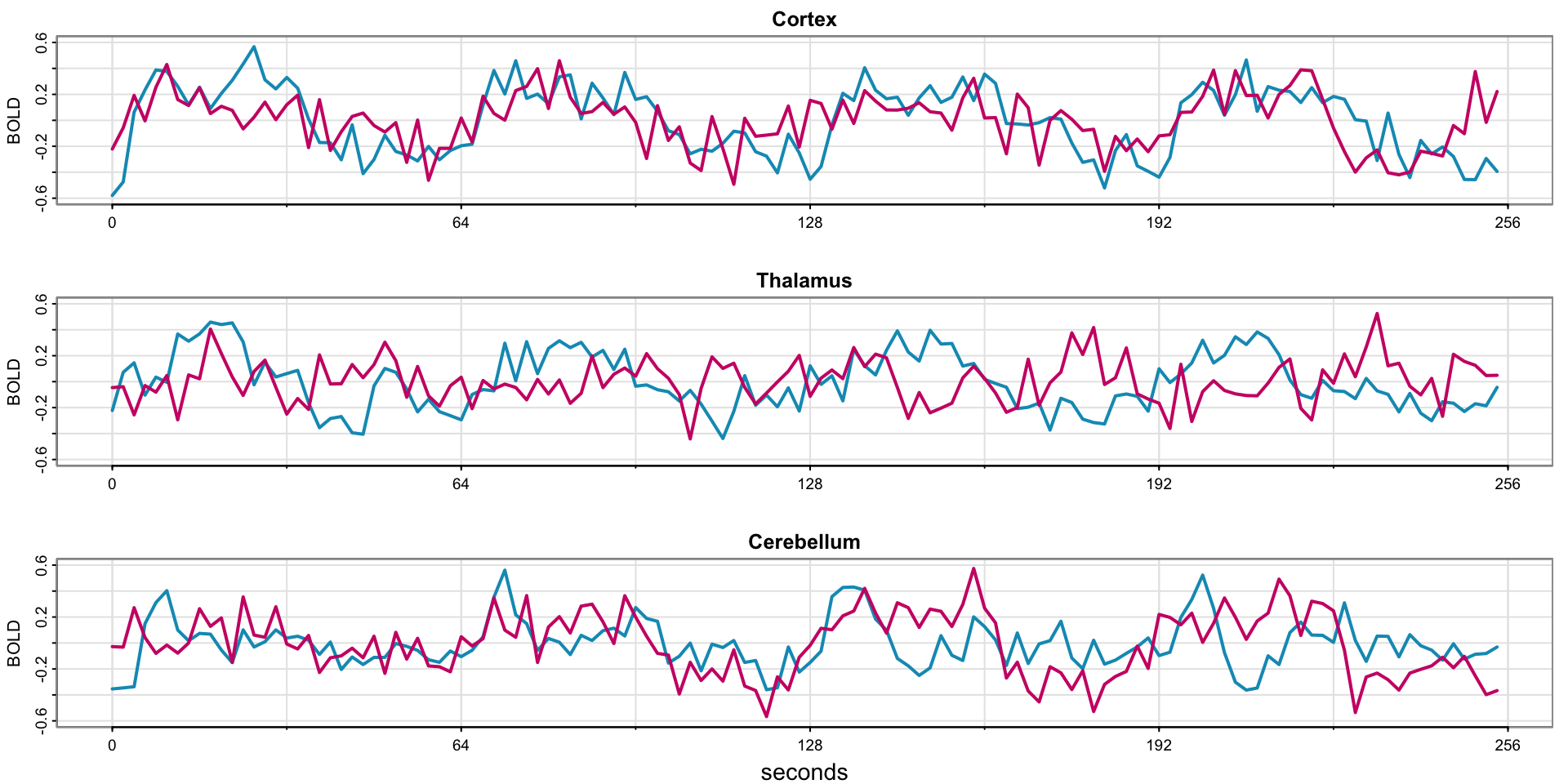

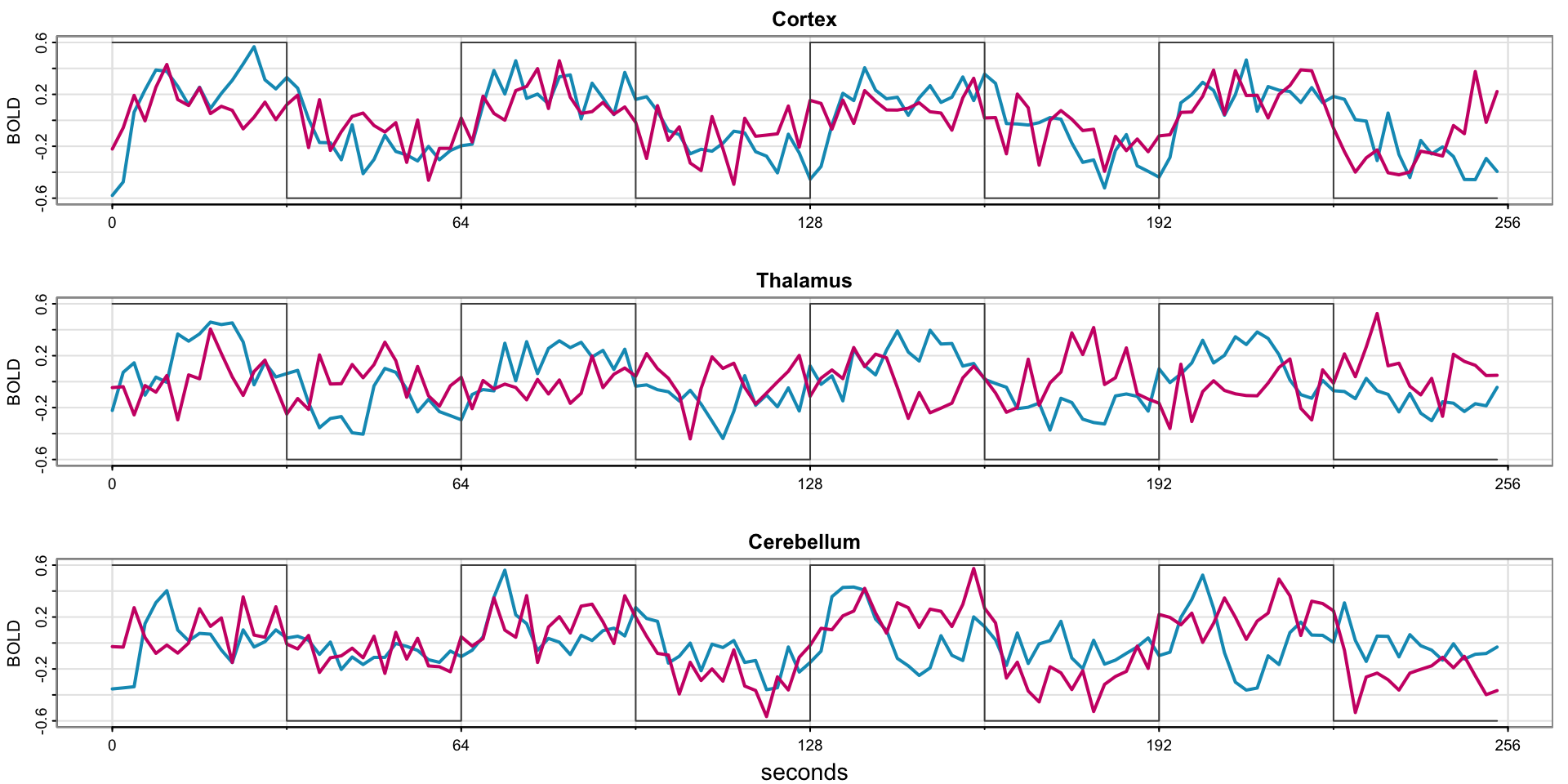

Example 1.6 fMRI Imaging

Code

par(mfrow=c(3,1))

x = ts(fmri1[,4:9], start=0, freq=32) # data

names = c("Cortex","Thalamus","Cerebellum")

u = ts(rep(c(rep(.6,16), rep(-.6,16)), 4), start=0, freq=32) # stimulus signal

for (i in 1:3){

j = 2*i-1

tsplot(x[,j:(j+1)], ylab="BOLD", xlab="", main=names[i], col=5:6, ylim=c(-.6,.6),

lwd=2, xaxt="n", spaghetti=TRUE)

axis(seq(0,256,64), side=1, at=0:4)

#lines(u, type="s", col=gray(.3))

}

mtext("seconds", side=1, line=1.75, cex=.9)

Code

par(mfrow=c(3,1))

x = ts(fmri1[,4:9], start=0, freq=32) # data

names = c("Cortex","Thalamus","Cerebellum")

u = ts(rep(c(rep(.6,16), rep(-.6,16)), 4), start=0, freq=32) # stimulus signal

for (i in 1:3){

j = 2*i-1

tsplot(x[,j:(j+1)], ylab="BOLD", xlab="", main=names[i], col=5:6, ylim=c(-.6,.6),

lwd=2, xaxt="n", spaghetti=TRUE)

axis(seq(0,256,64), side=1, at=0:4)

lines(u, type="s", col=gray(.3))

}

mtext("seconds", side=1, line=1.75, cex=.9)

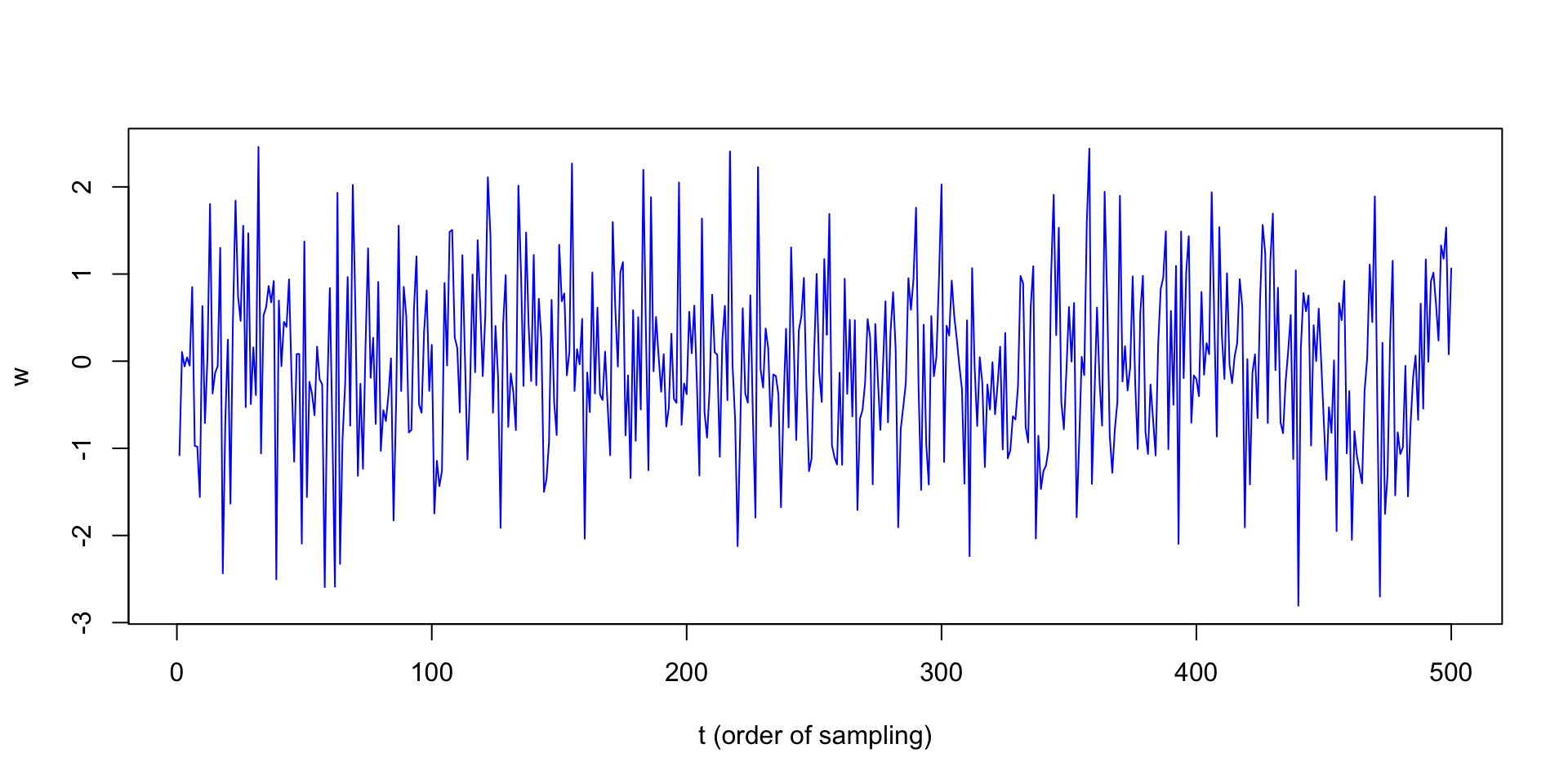

Plotting White Noise

Which example does this bear the most resemblance to?

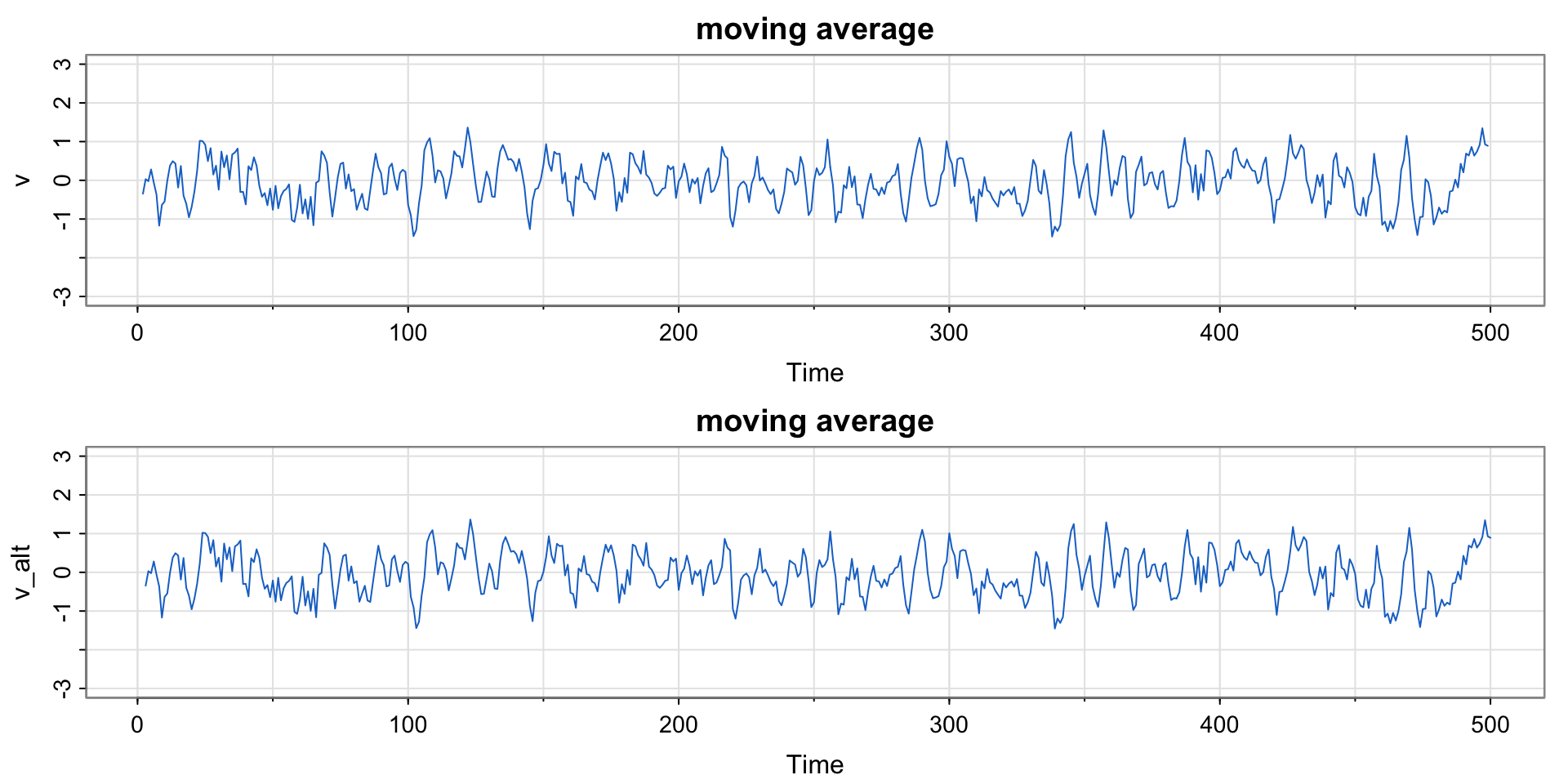

Plotting a Moving Average

Compare this moving average to the SOI and Recruitment series. How do they differ?

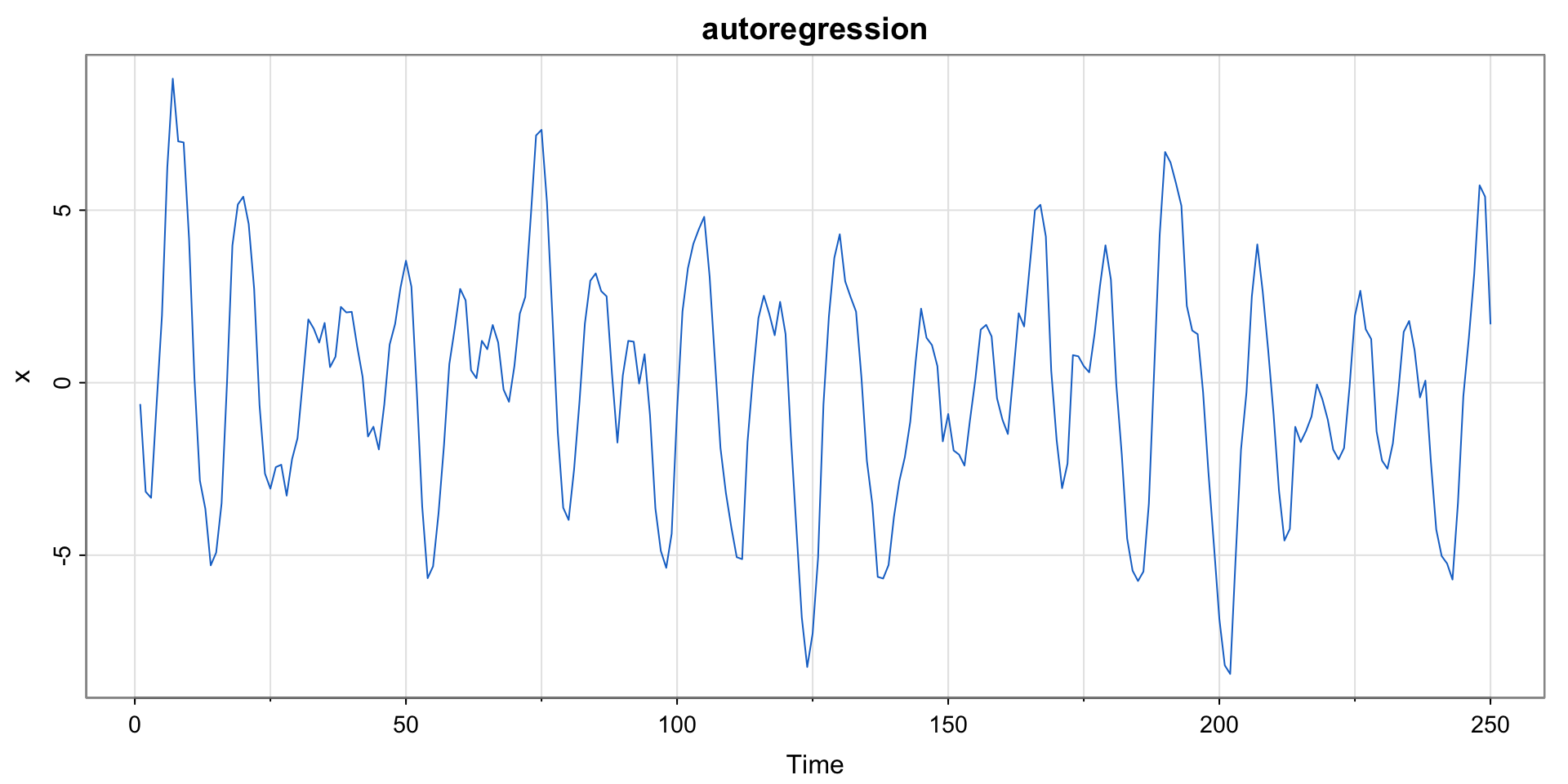

Plotting Autoregressions

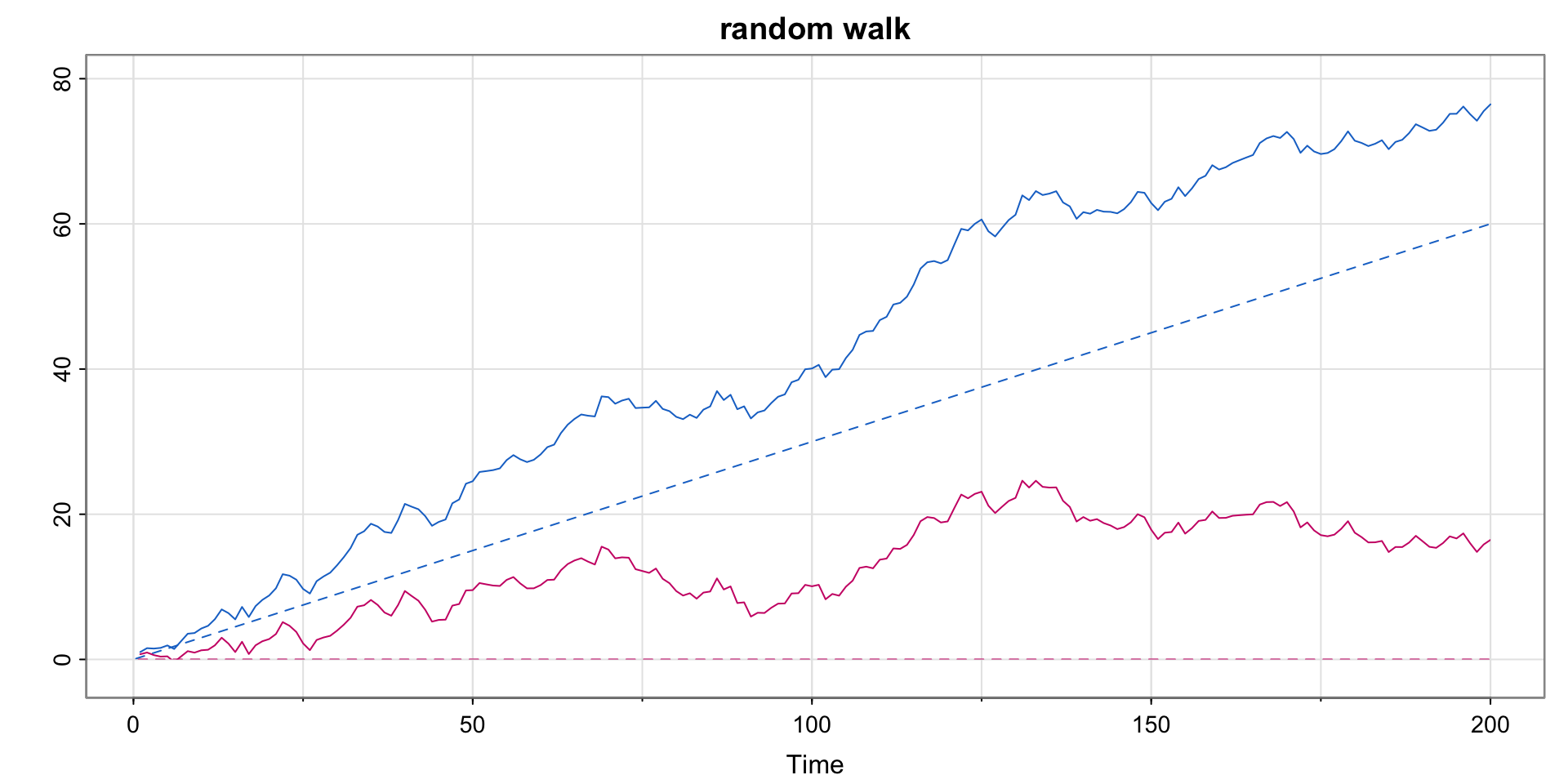

Plotting a Random Walk with Drift

Code

set.seed(314159265) # so you can reproduce the results

w = rnorm(200) ## Gaussian white noise

x = cumsum(w)

wd = w +.3

xd = cumsum(wd)

tsplot(xd, ylim=c(-2,80), main="random walk", ylab="", col=4)

clip(0, 200, 0, 80)

abline(a=0, b=.3, lty=2, col=4) # drift

lines(x, col=6)

clip(0, 200, 0, 80)

abline(h=0, col=6, lty=2)

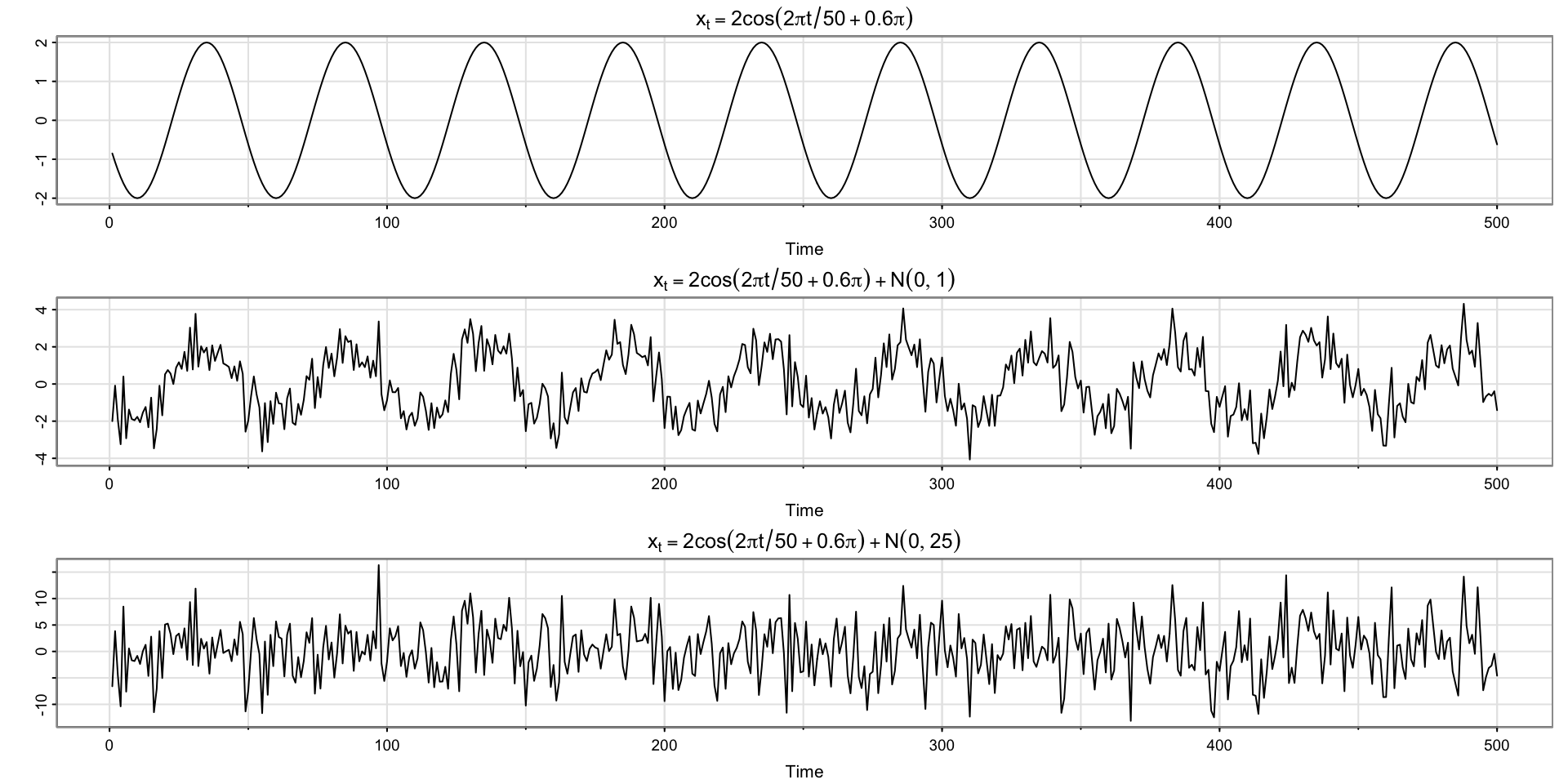

Plotting Signal Plus Noise (two scenarios)

Code

# cs = 2*cos(2*pi*(1:500)/50 + .6*pi) # as in the text

cs = 2*cos(2*pi*(1:500+15)/50) # same thing

w = rnorm(500,0,1)

par(mfrow=c(3,1))

tsplot(cs, ylab="", main = expression(x[t]==2*cos(2*pi*t/50+.6*pi)))

tsplot(cs + w, ylab="", main = expression(x[t]==2*cos(2*pi*t/50+.6*pi)+N(0,1)))

tsplot(cs + 5*w, ylab="", main = expression(x[t]==2*cos(2*pi*t/50+.6*pi)+N(0,25)))