Both simplify to \[

\gamma(h) = \begin{cases}

26 & \Vert h \Vert = 0 \\

5 & \Vert h \Vert = 1 \\

0 & \Vert h \Vert > 1

\end{cases}

\]

In practice we cannot distinguish the difference between the two models (they are stochastically the same). So, we will choose the invertible model, which is the one with \(\sigma^2_w =25\), \(\theta = 1/5\) (see Shumway and Stoffer page 72-73, example 4.6 for details.)

Interpretation of ARMA model

If we let \(\epsilon_t = w_t + \theta_1 w_{t-1} + \theta_2 w_{t-2} + \dots + \theta_q w_{t-q}\), then if \(x_t\) is ARMA(p,q), \[

x_t = \alpha + \phi_1 x_{t-1} + \phi_2 x_{t-2} + \dots + \phi_p x_{t-p} + \epsilon_t

\]

Recognize the linear regression structure?

Difference: constraints on \(\phi, \theta\).

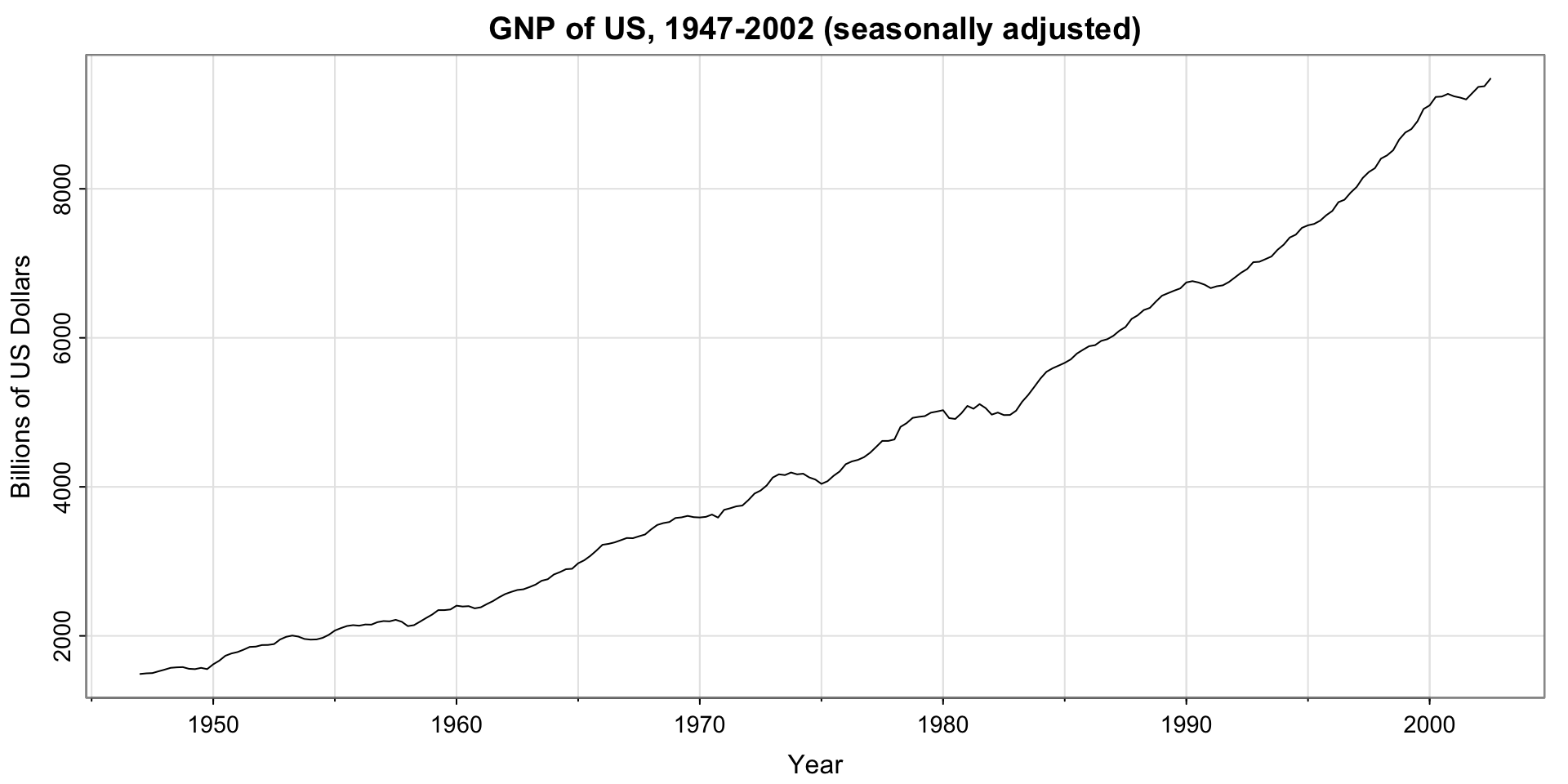

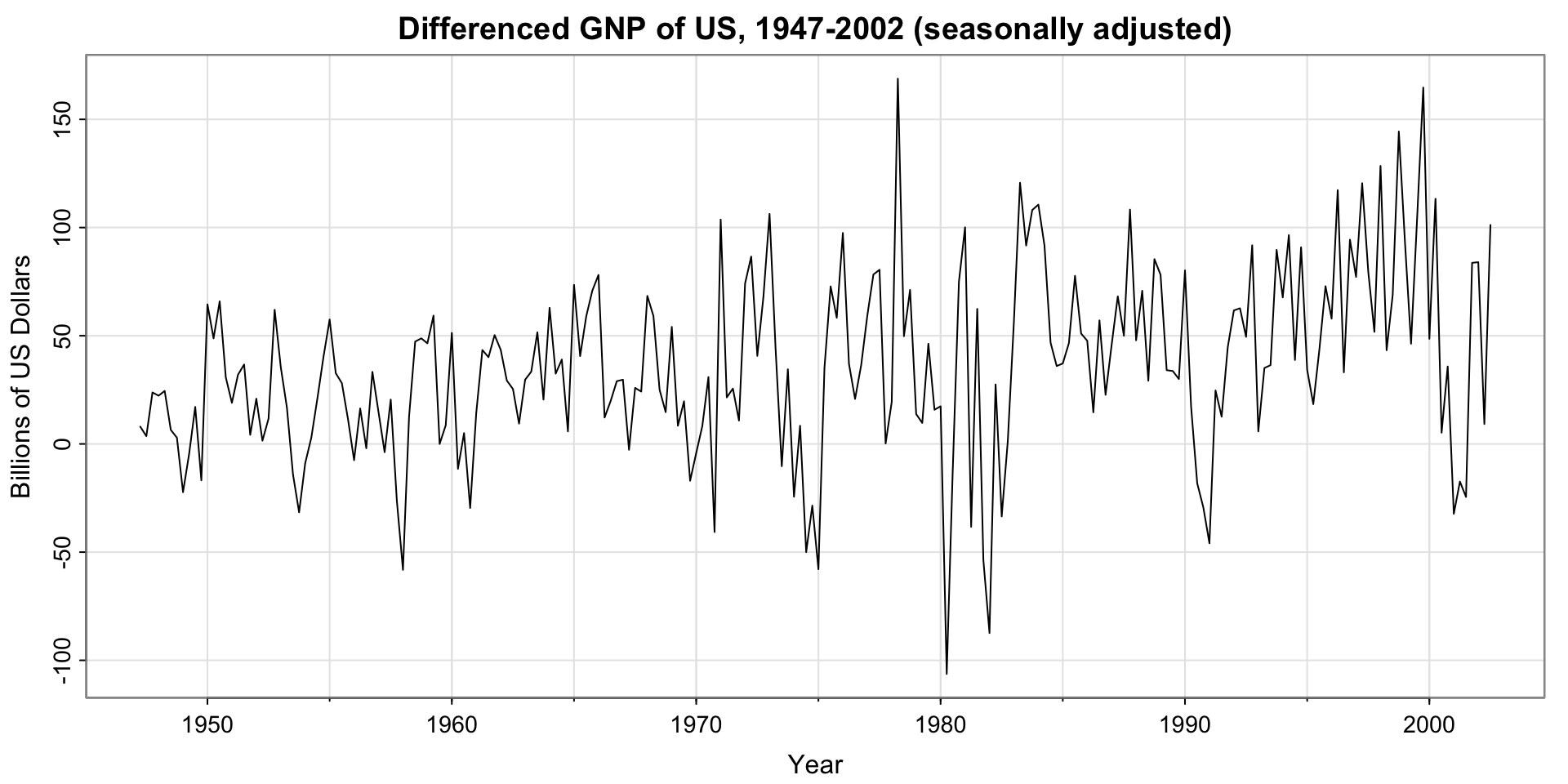

Activity 2: Fit an ARMA model?

Is there any seasonality (fixed-length cycles)? If so, probably want to use a seasonal model (not ARMA)

Activity 2 Solution: Fit an ARMA model?

No, the cycles are not of fixed length

[1] 15 12 17

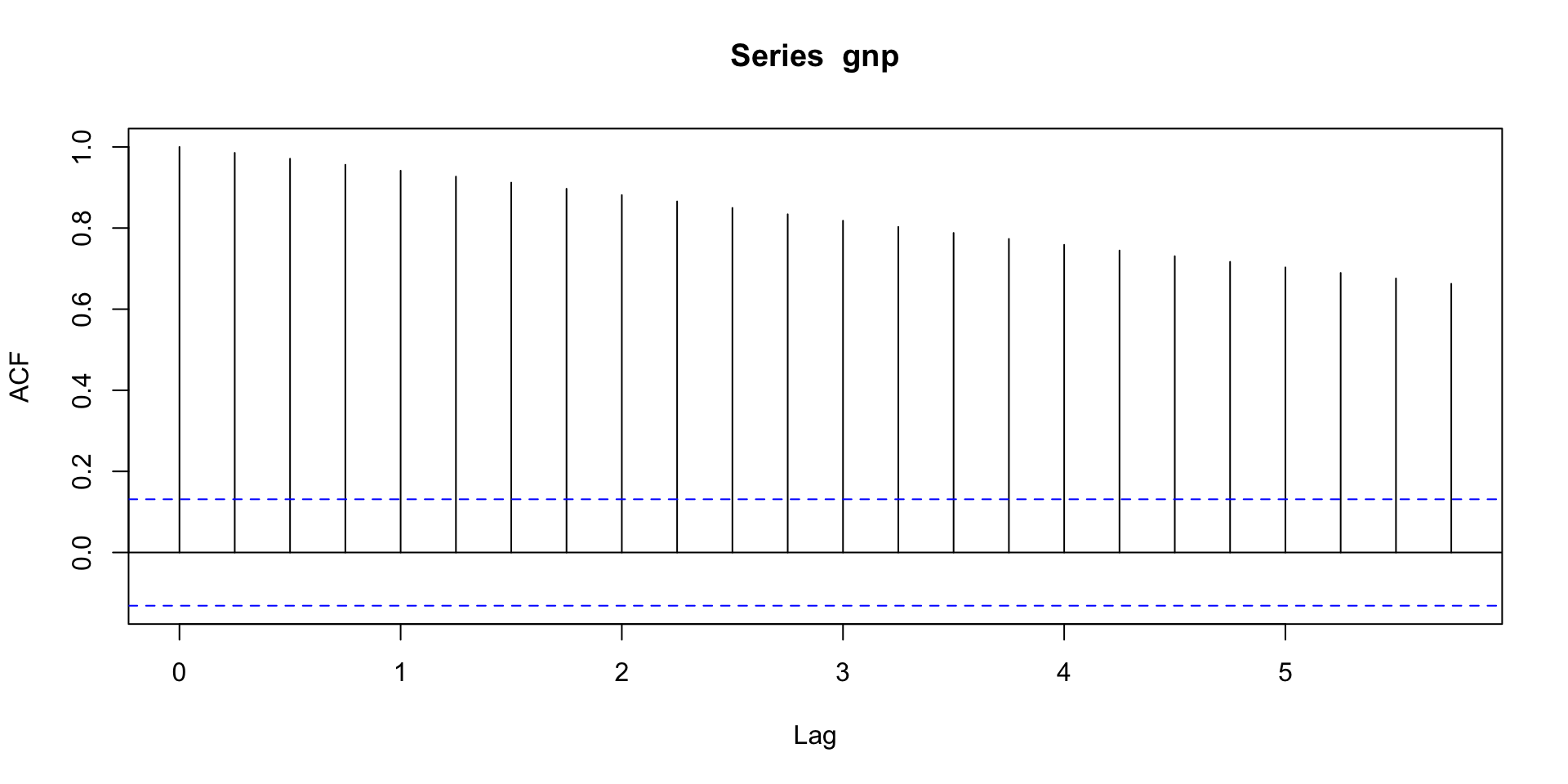

Choosing the order of ARMA models

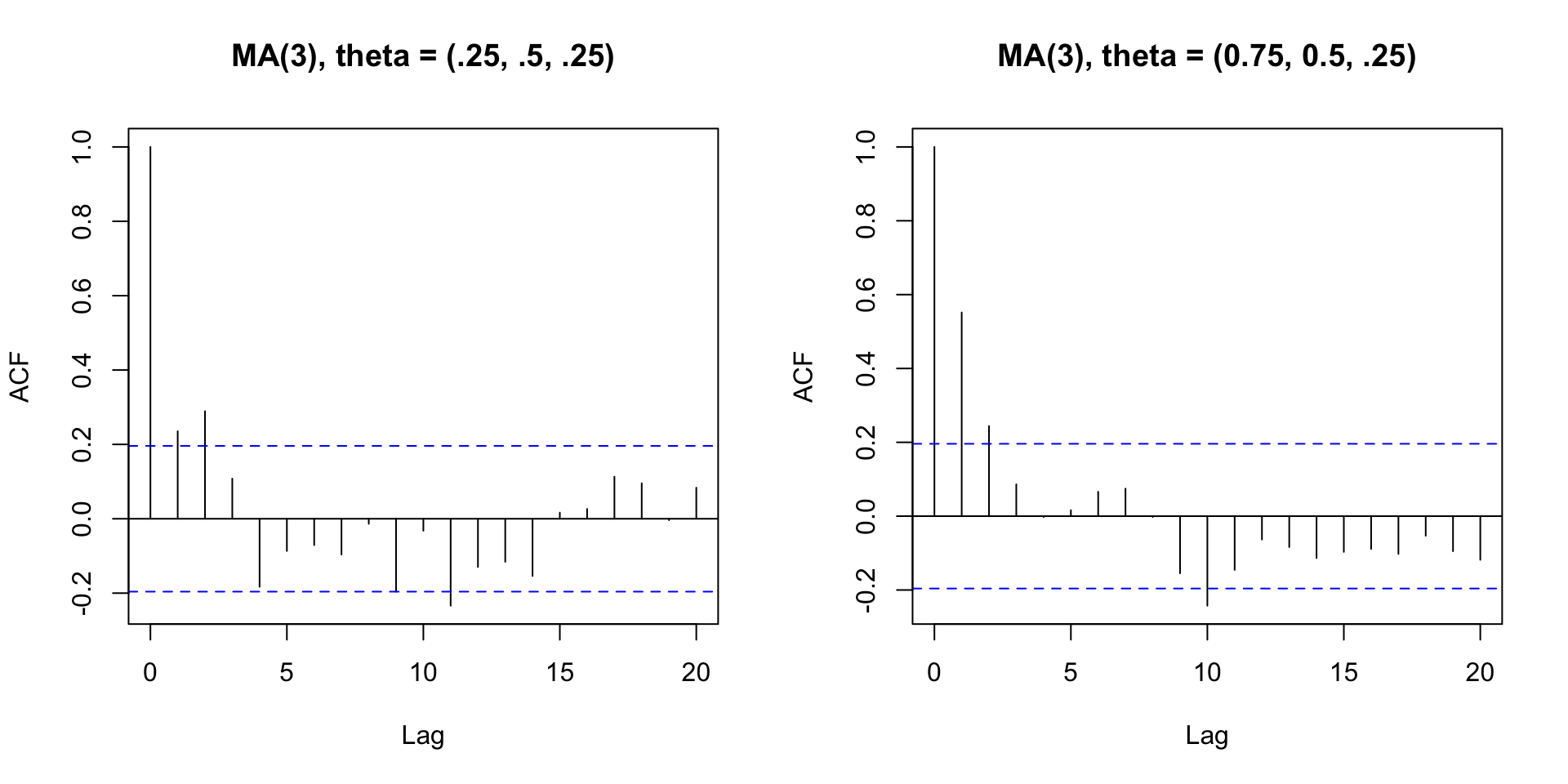

Activity 3: Recall MA ACF

Propose a rule for choosing the order of the MA model.

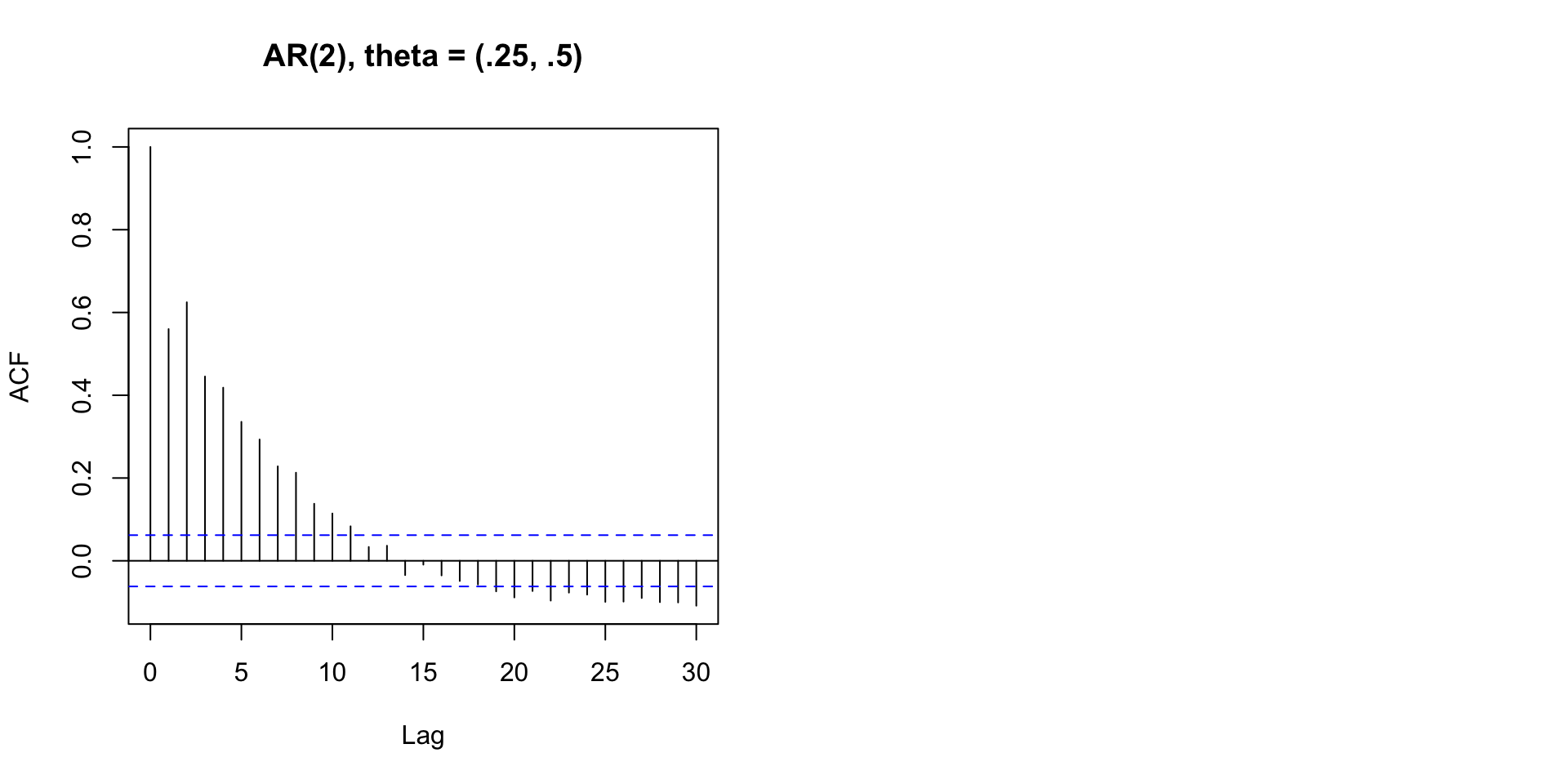

What about AR?

Error in arima.sim(list(ar = c(0.75, 0.5)), n = 1000): 'ar' part of model is not stationary

Activity 4: Fix the AR model so it is stationary

Code

set.seed(807)par(mfrow =c(1,2))acf(arima.sim(list(ar =c(0.25, 0.5)), n =1000), main ="AR(2), theta = (.25, .5)")acf(arima.sim(list(ar =c(FIXME, FIXME)), n =1000),main ="AR(2), theta = (FIX, FIX)") #hint (lecture 1)

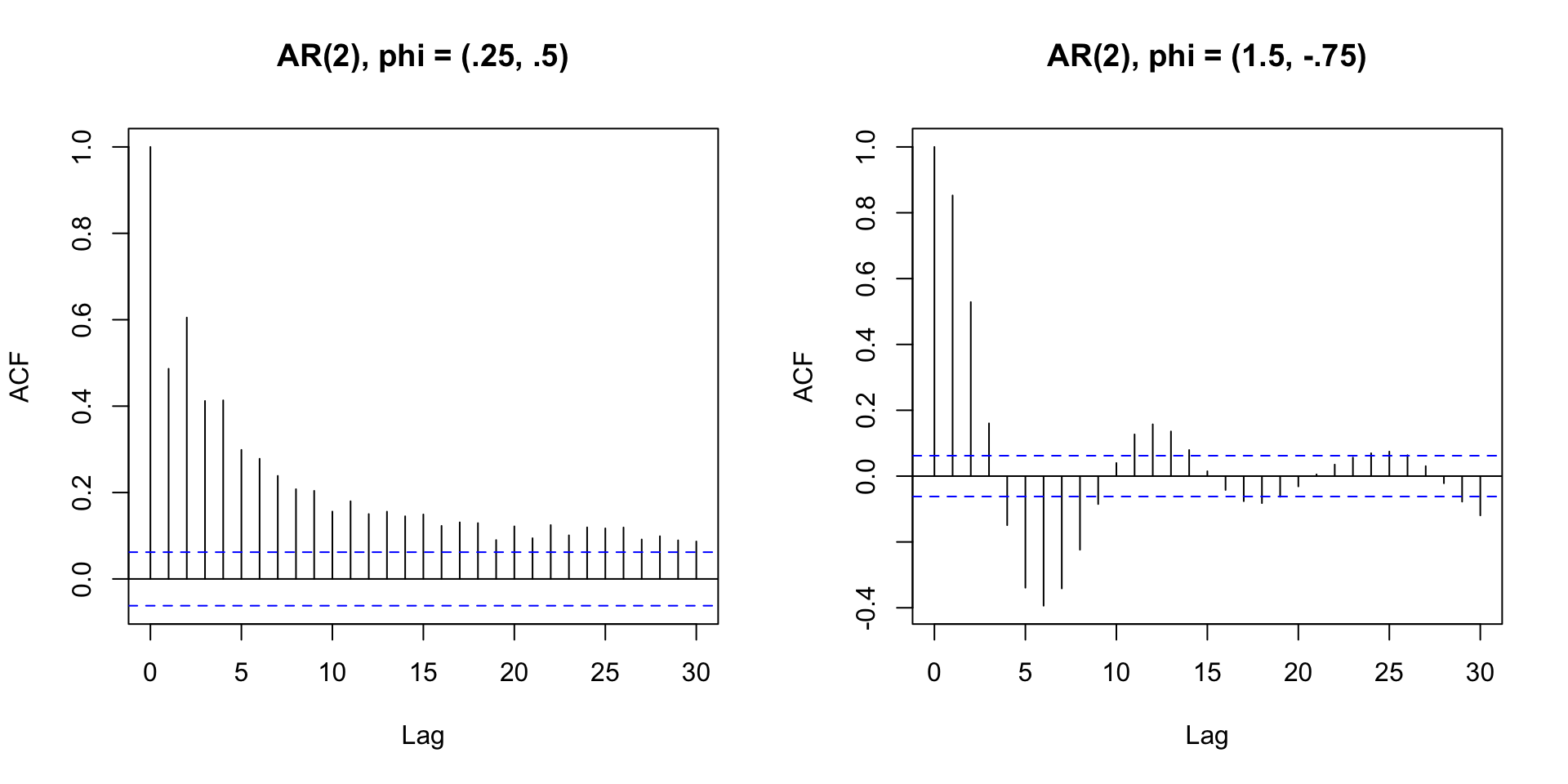

Activity 4 Solution: Fix the AR model so it is stationary

Making sure AR is stationary

Is complicated

Is taken care of in estimation by software

AR or MA or both?

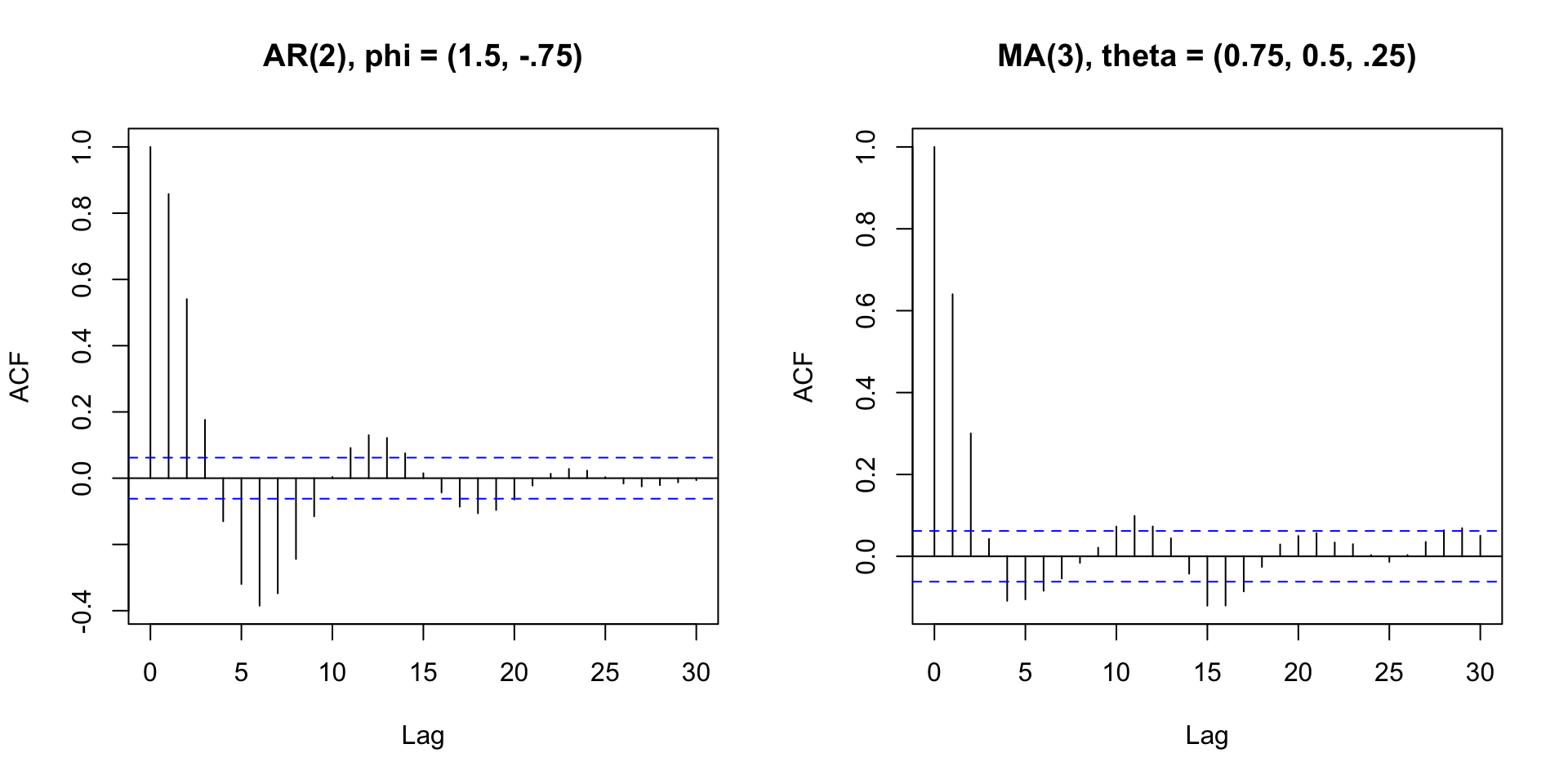

Consider two of the models just simulated:

Shape is similar, but not identical

Is there a better way to tell?

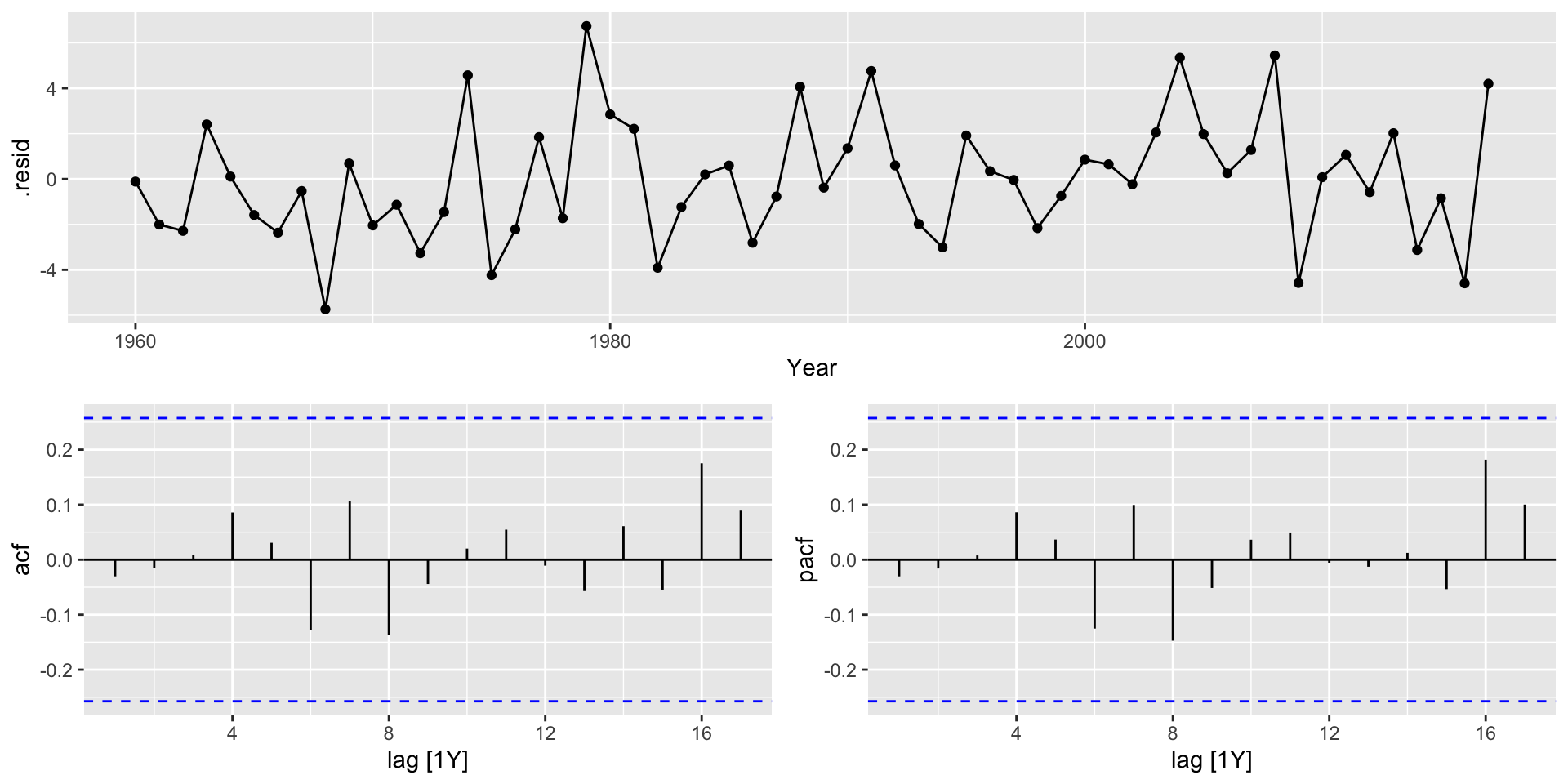

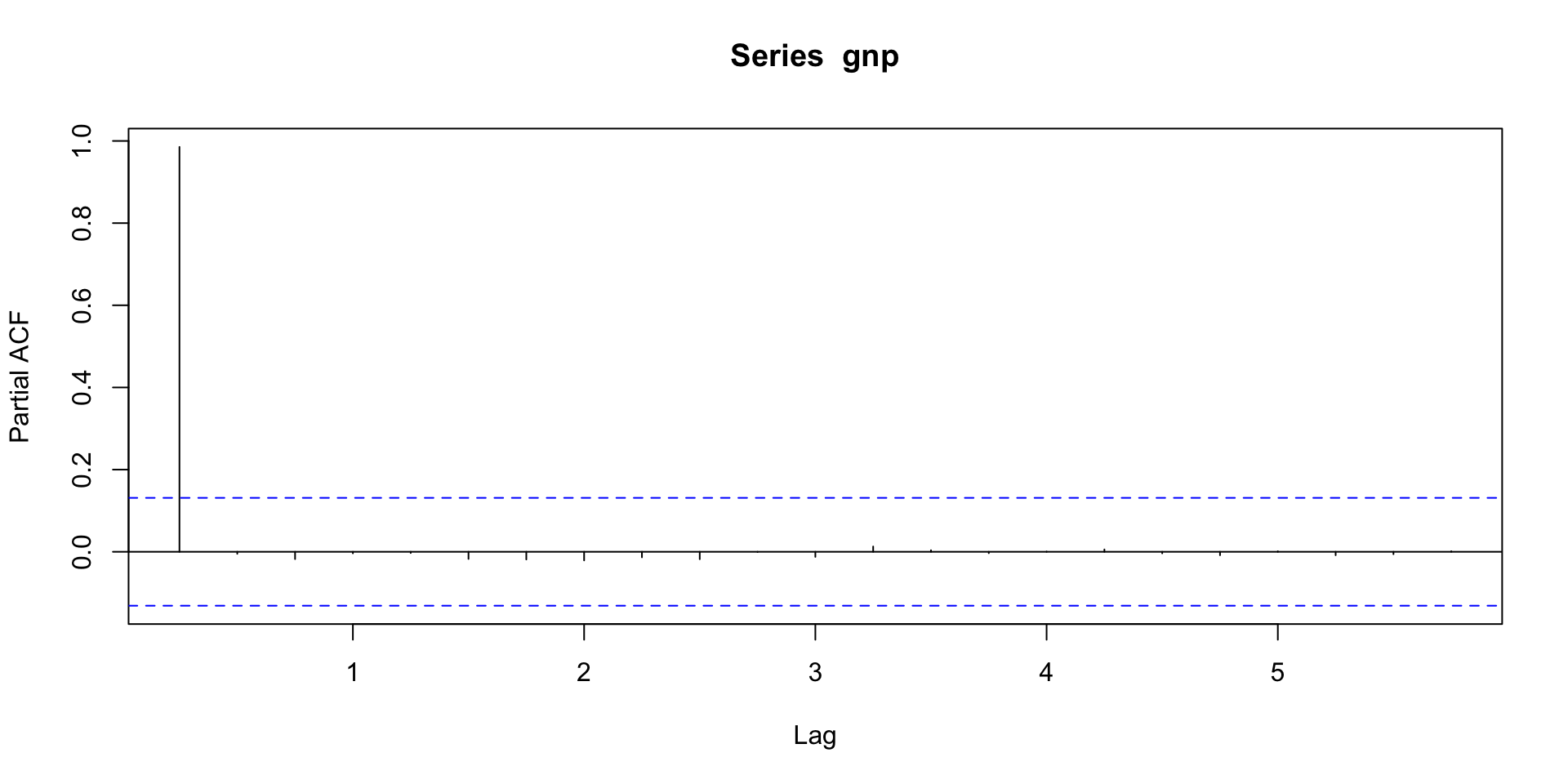

Partial Autocorrelation plot

The PACF is the correlation between \(x_t\) and \(x_{t-k}\) that is not explained by lags \(1, 2, \ldots, k-1\).

“Removes” the autocorrelation of the previous lags.

Useful in determining the order of an Autoregressive process, and in combination with ACF, choosing between an AR or an MA model.

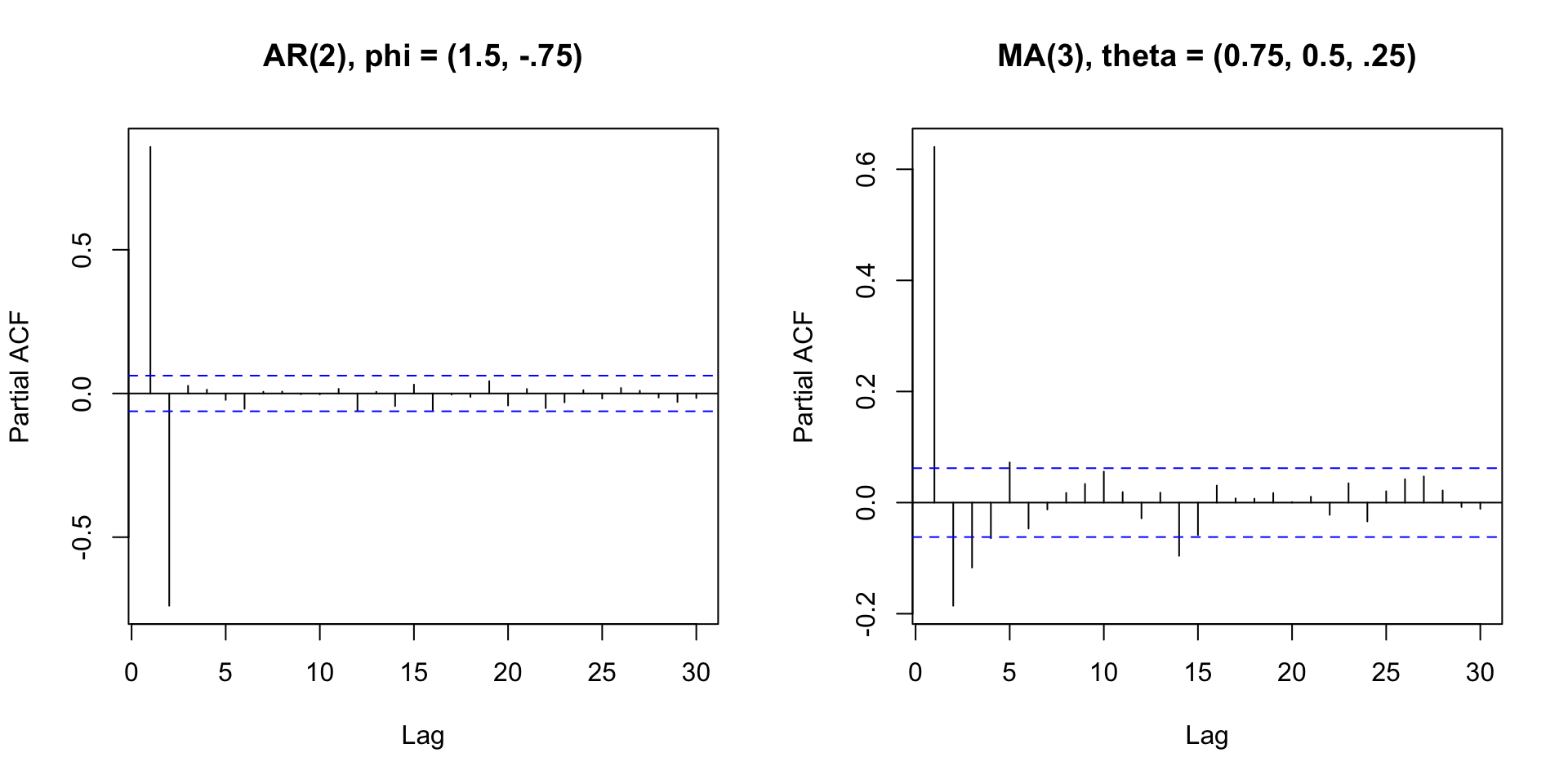

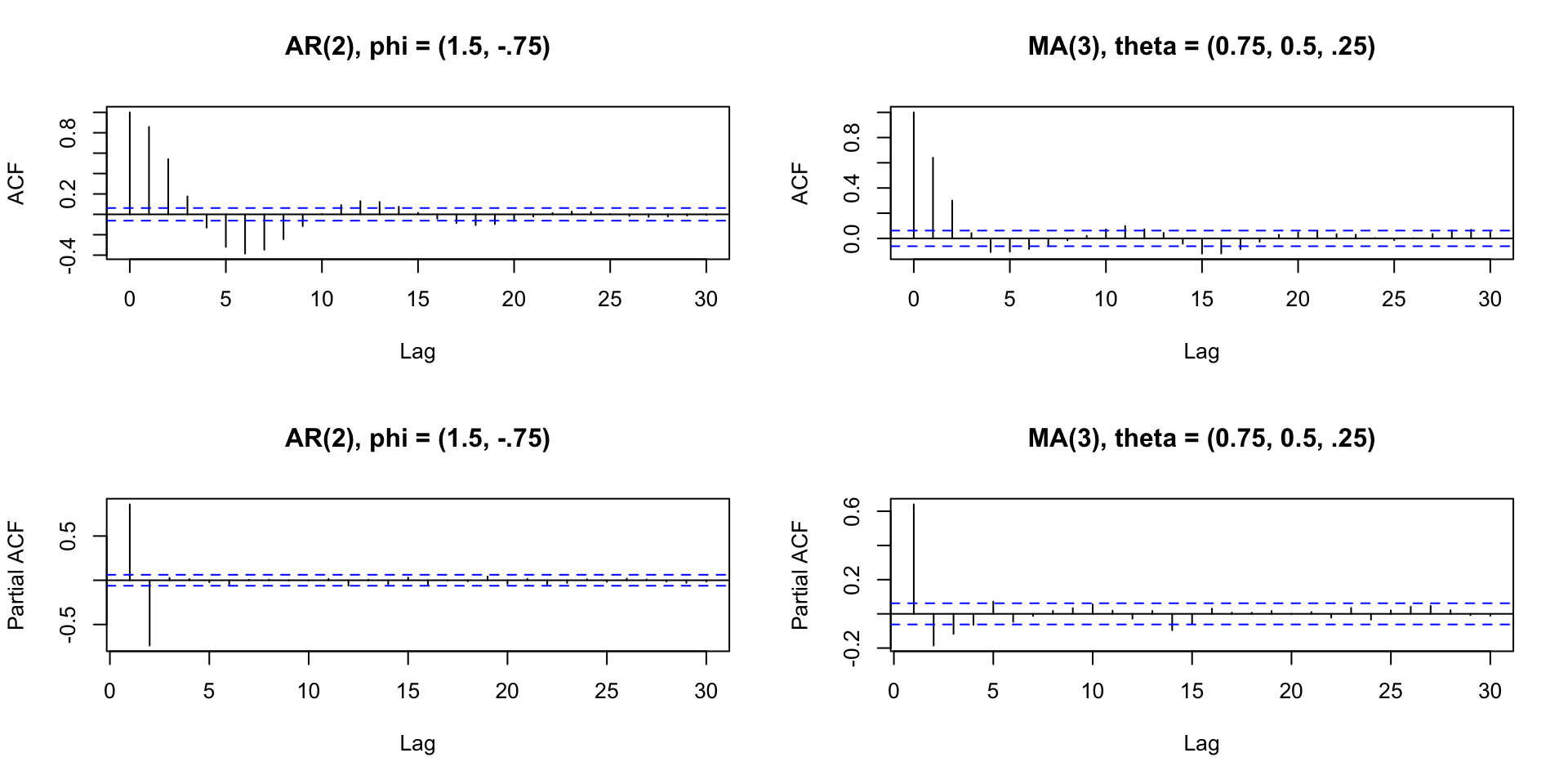

PACF of two series we just saw

ACF and PACF

AR or MA or both

Behavior of ACF/PACF for ARMA Models

AR(p)

MA(q)

ARMA(p,q)

ACF

Tails off

Cuts off after lag q

Tails off

PACF

Cuts off after lag p

Tails off

Tails off

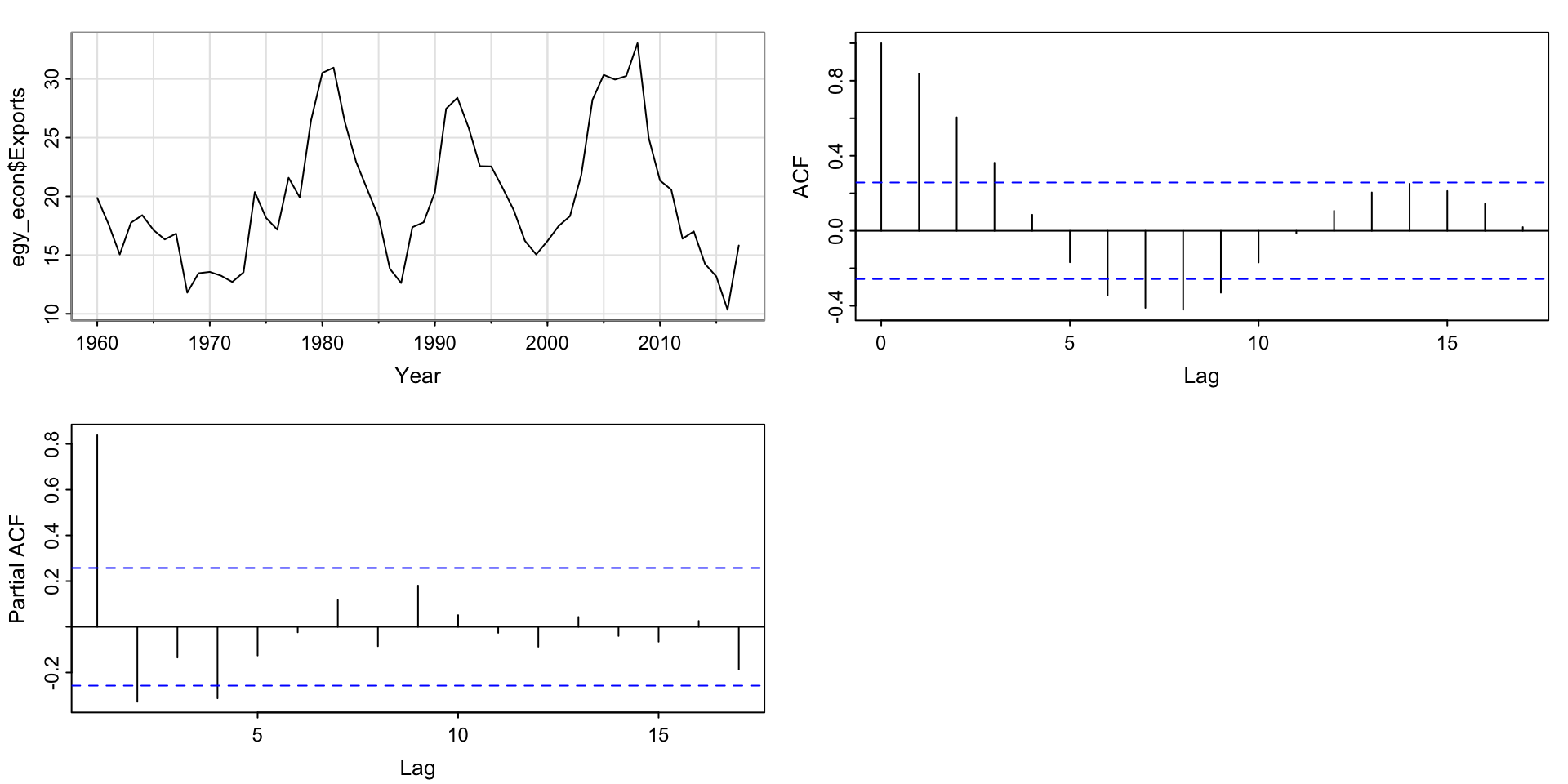

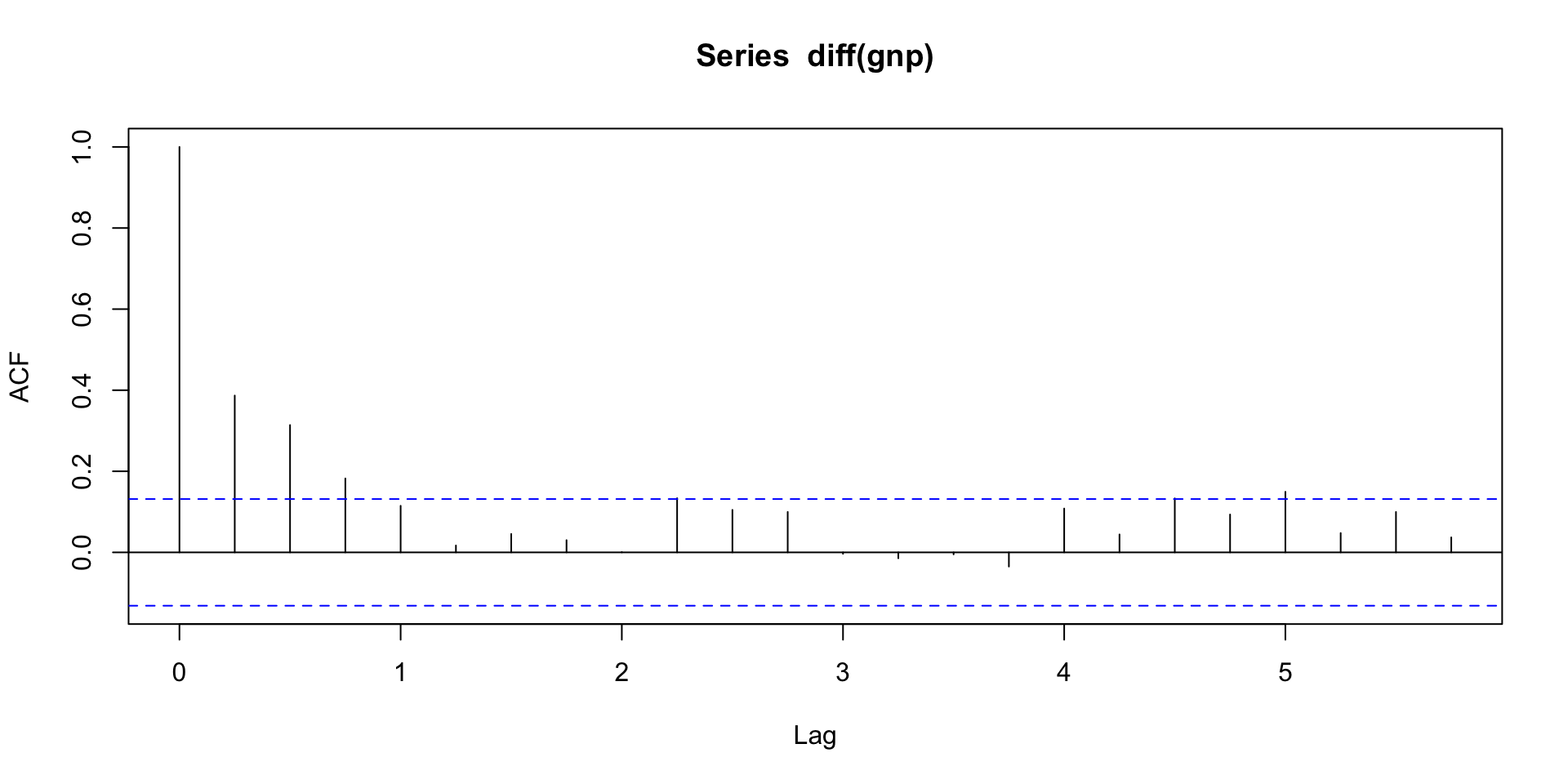

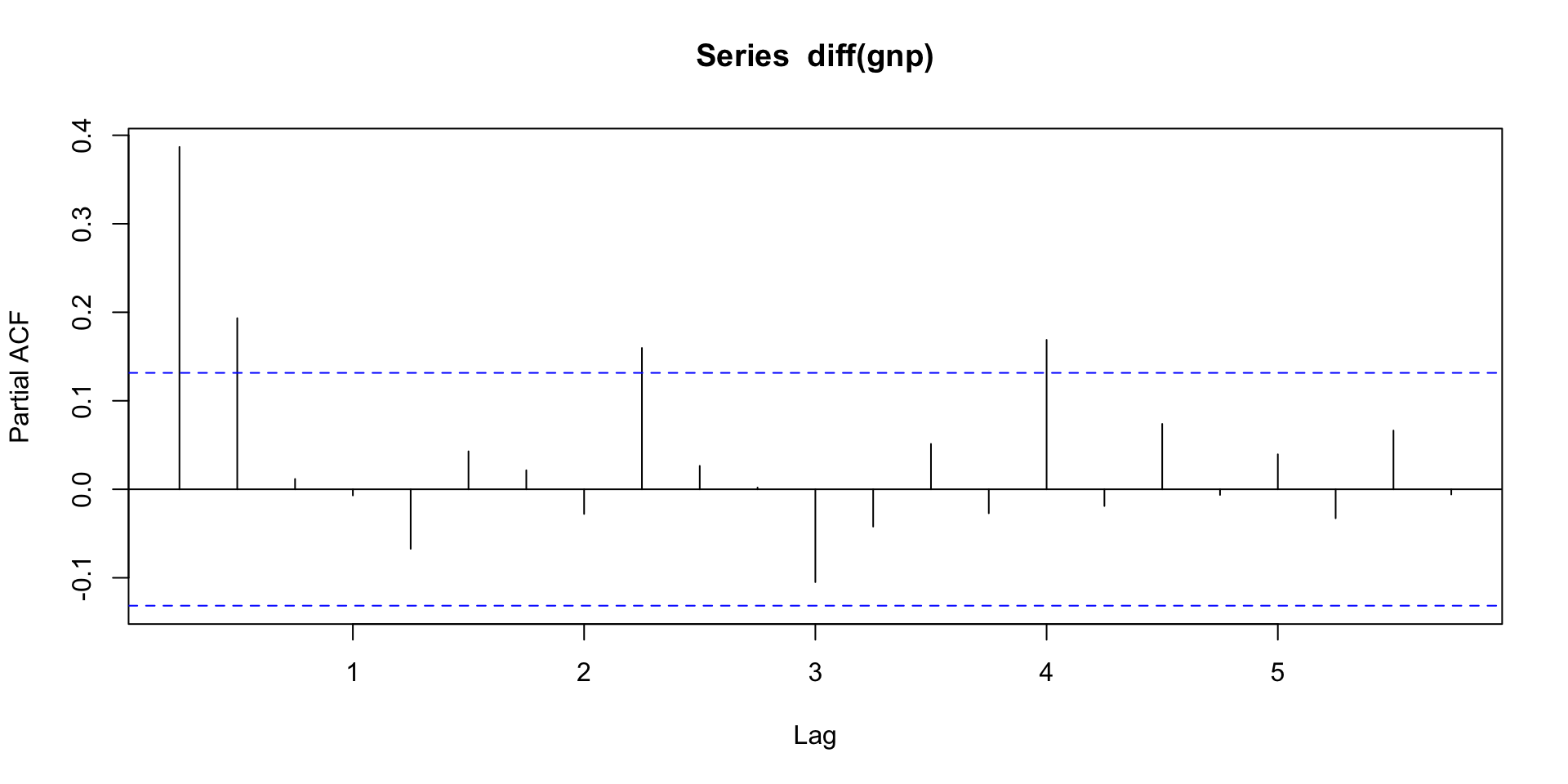

Activity 5: AR or MA or both?

ACF: Tails off; PACF: Cuts off after lag 4. Maybe an AR(4), or some sort of ARMA?

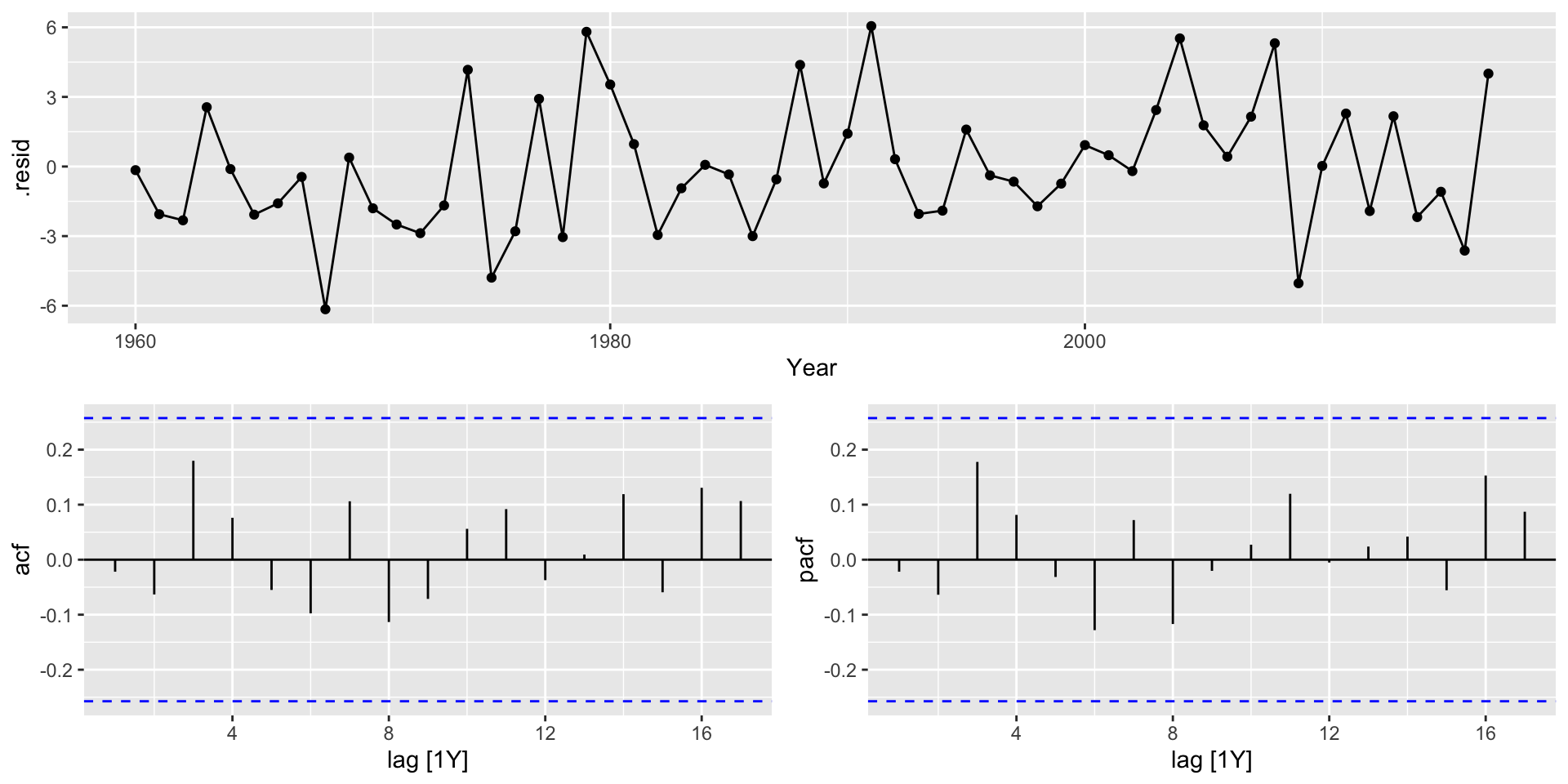

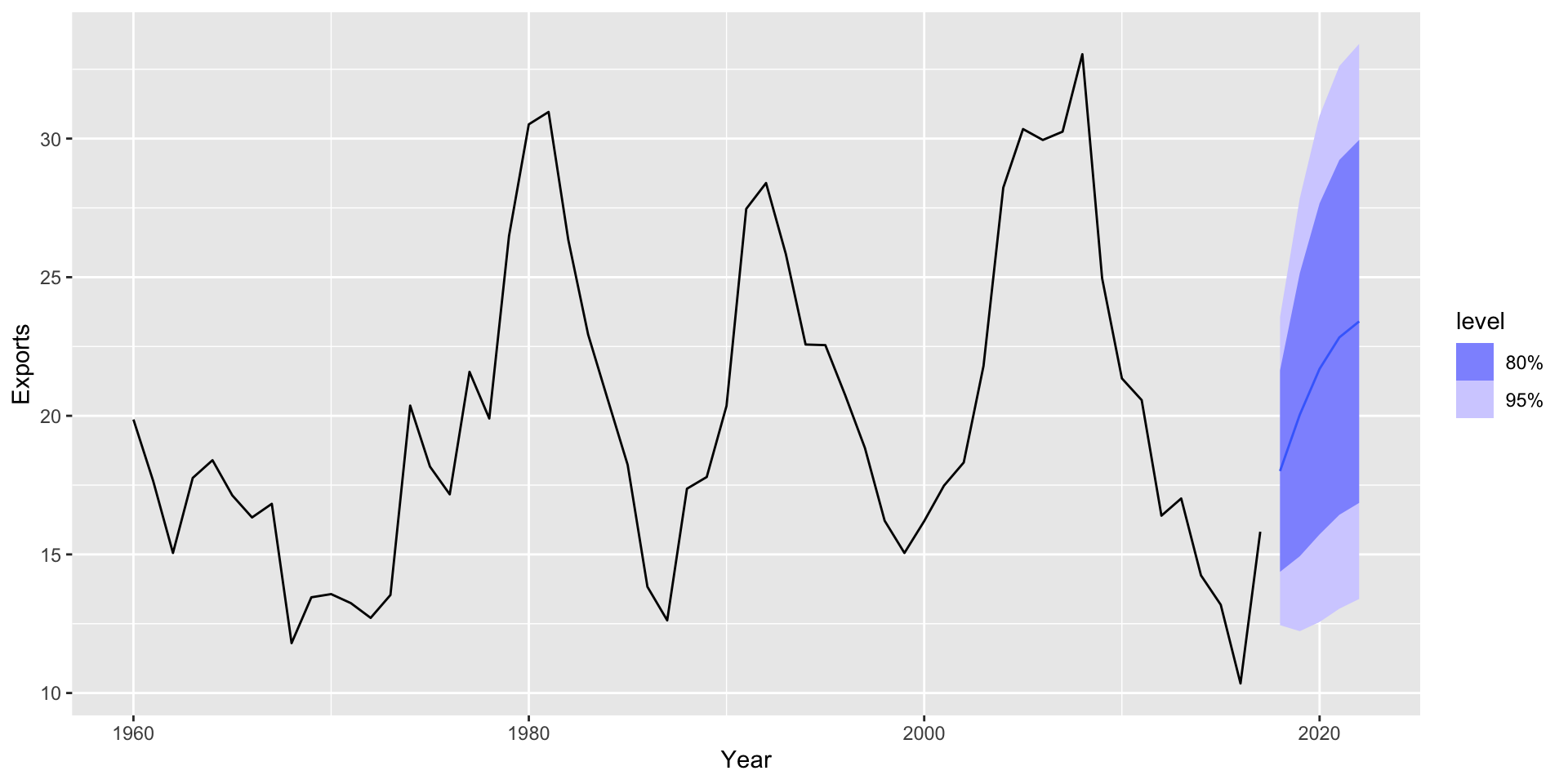

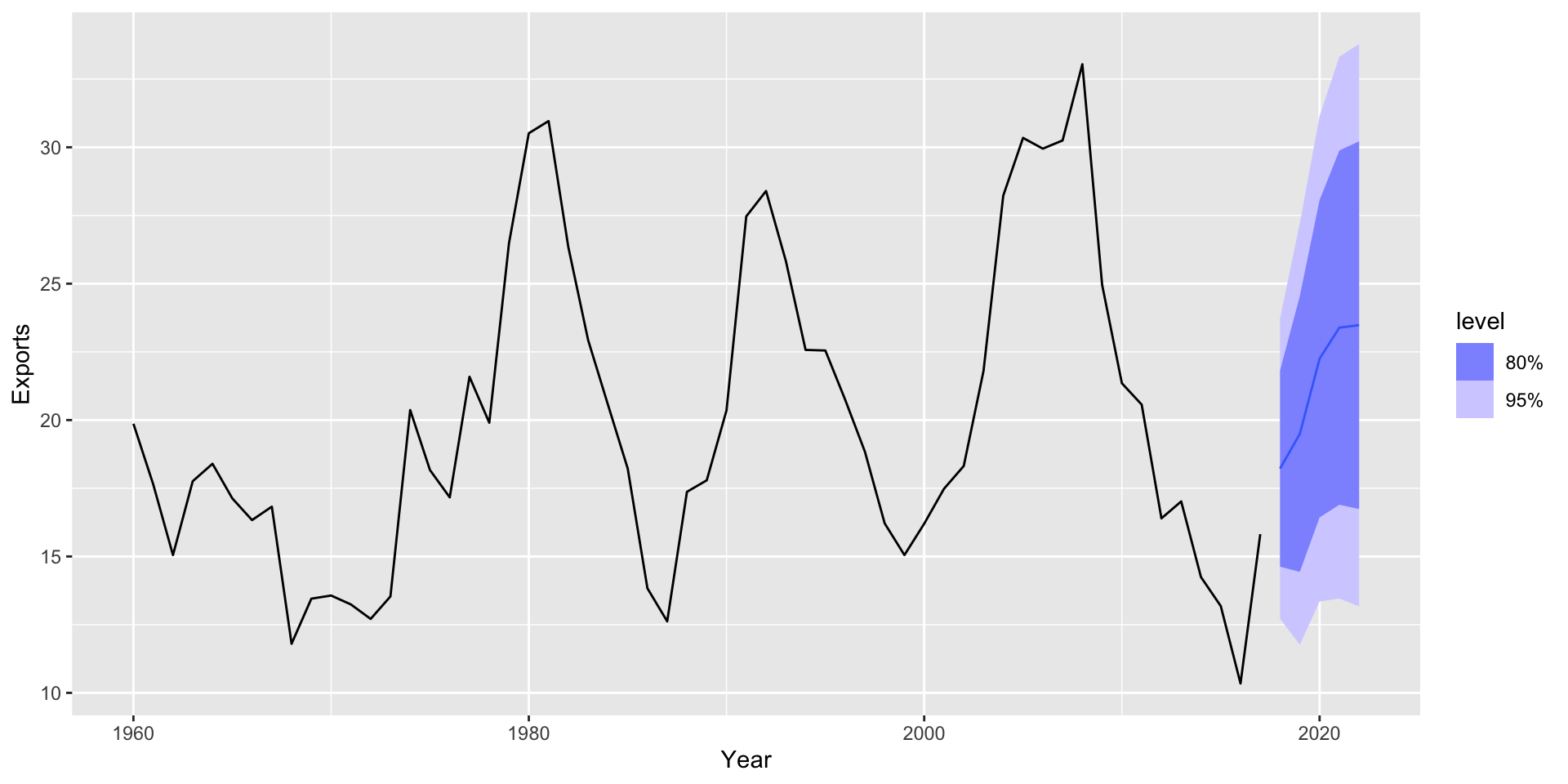

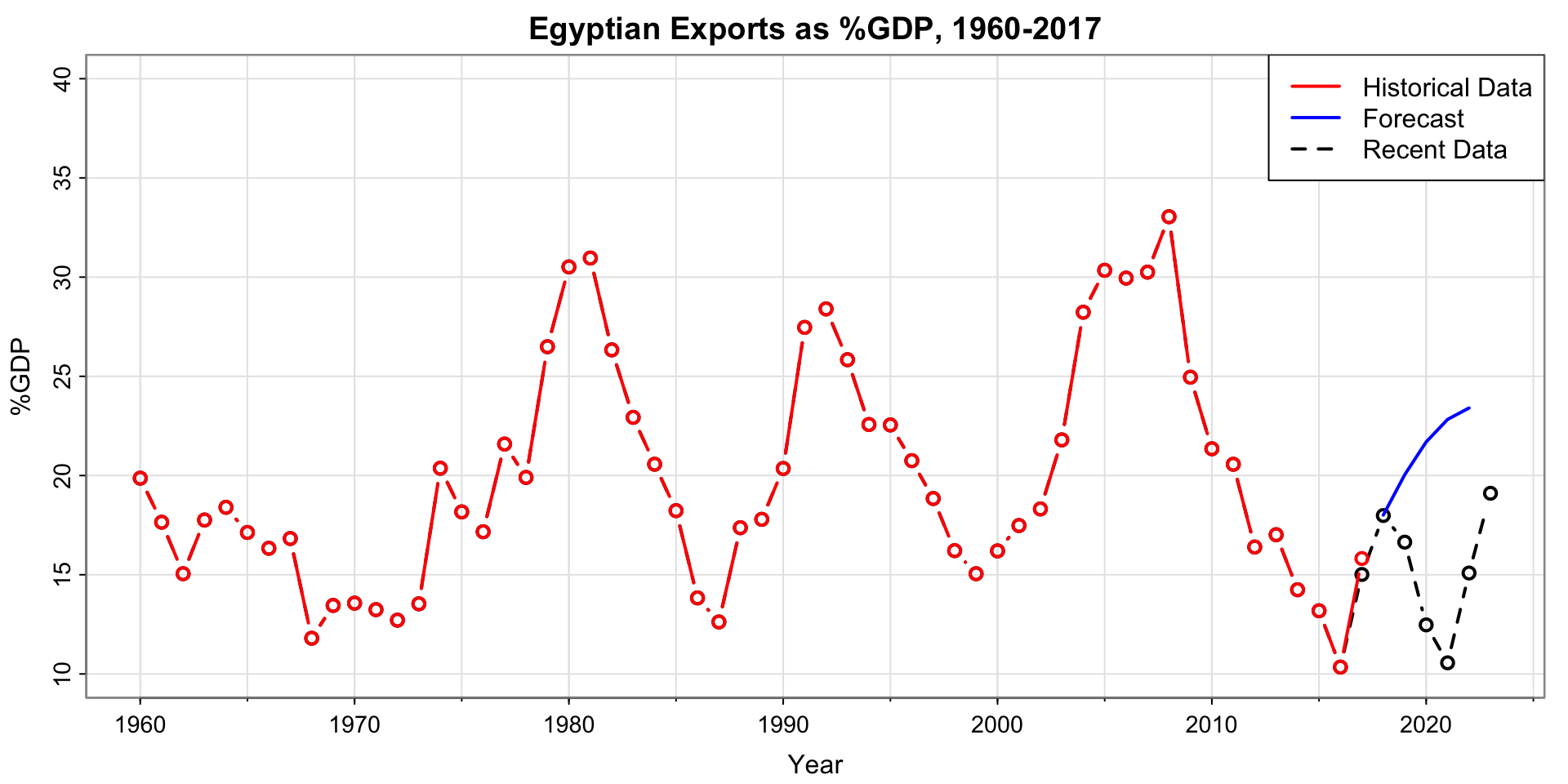

Fitting an ARMA model

Use the sarima function, specify p, d, q (d = 0 for ARMA).