Lecture 11

Last time

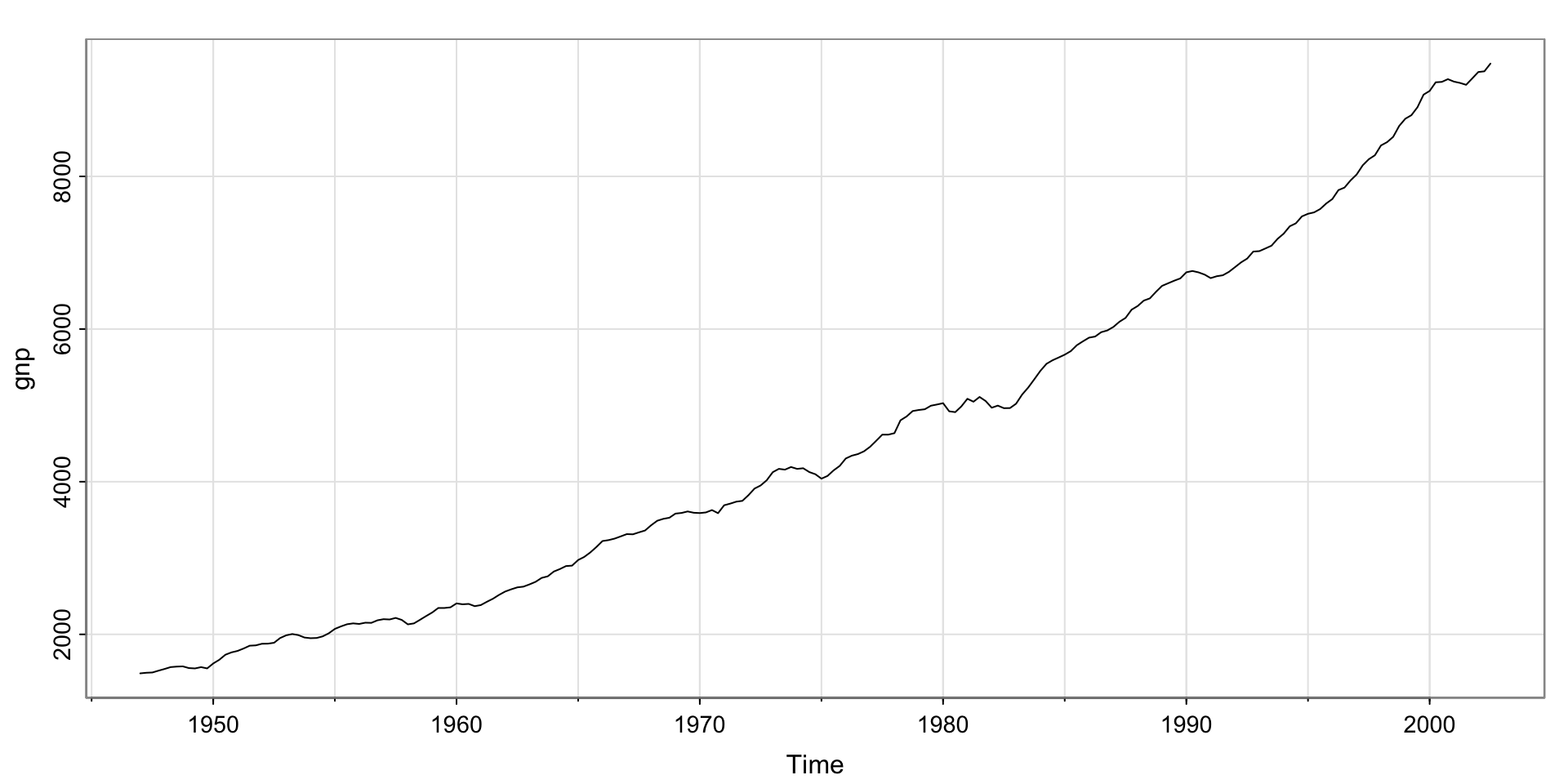

U.S. GNP data– clearly has a trend, nonstationary

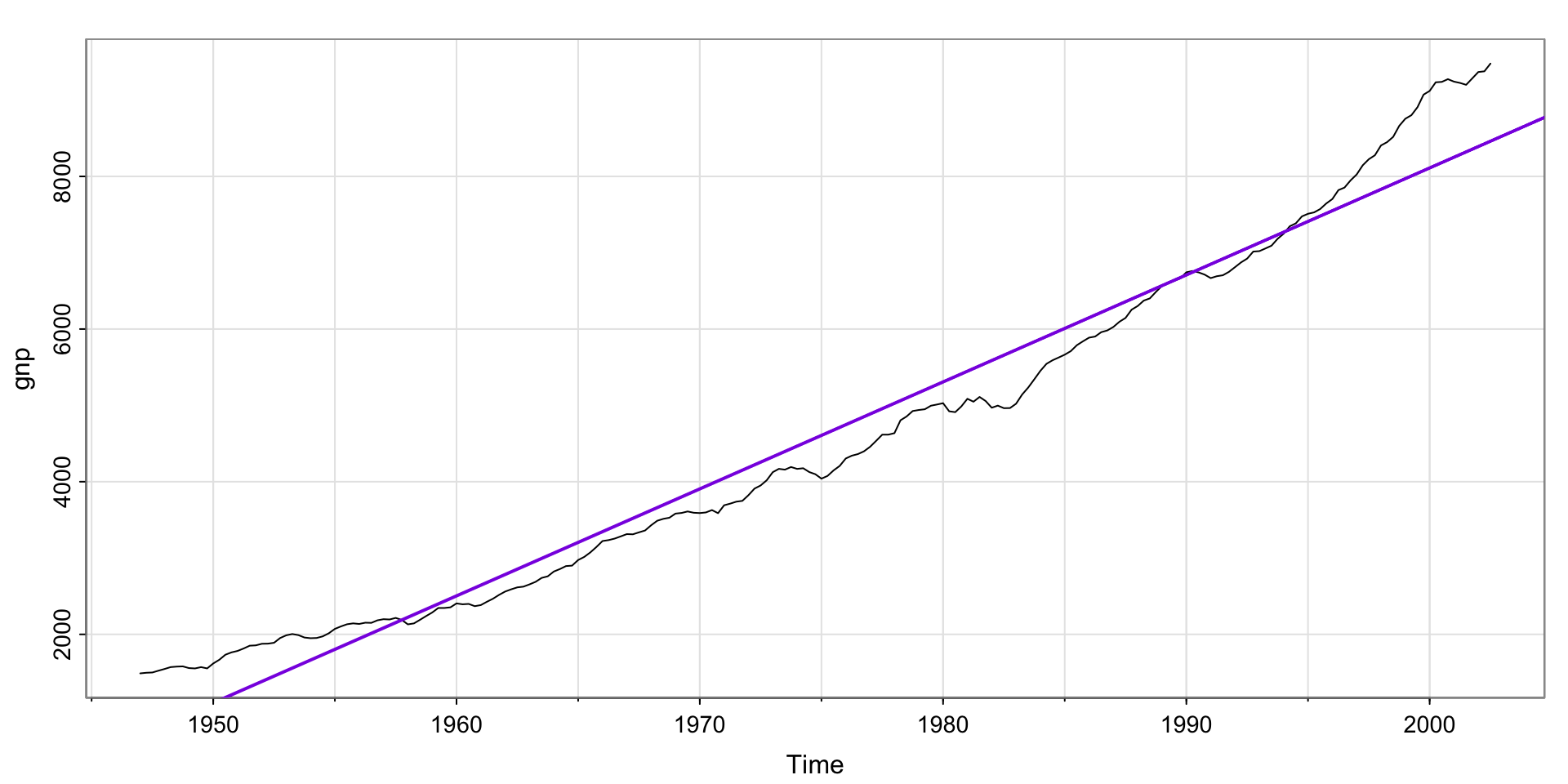

Is the trend linear?

Not exactly…

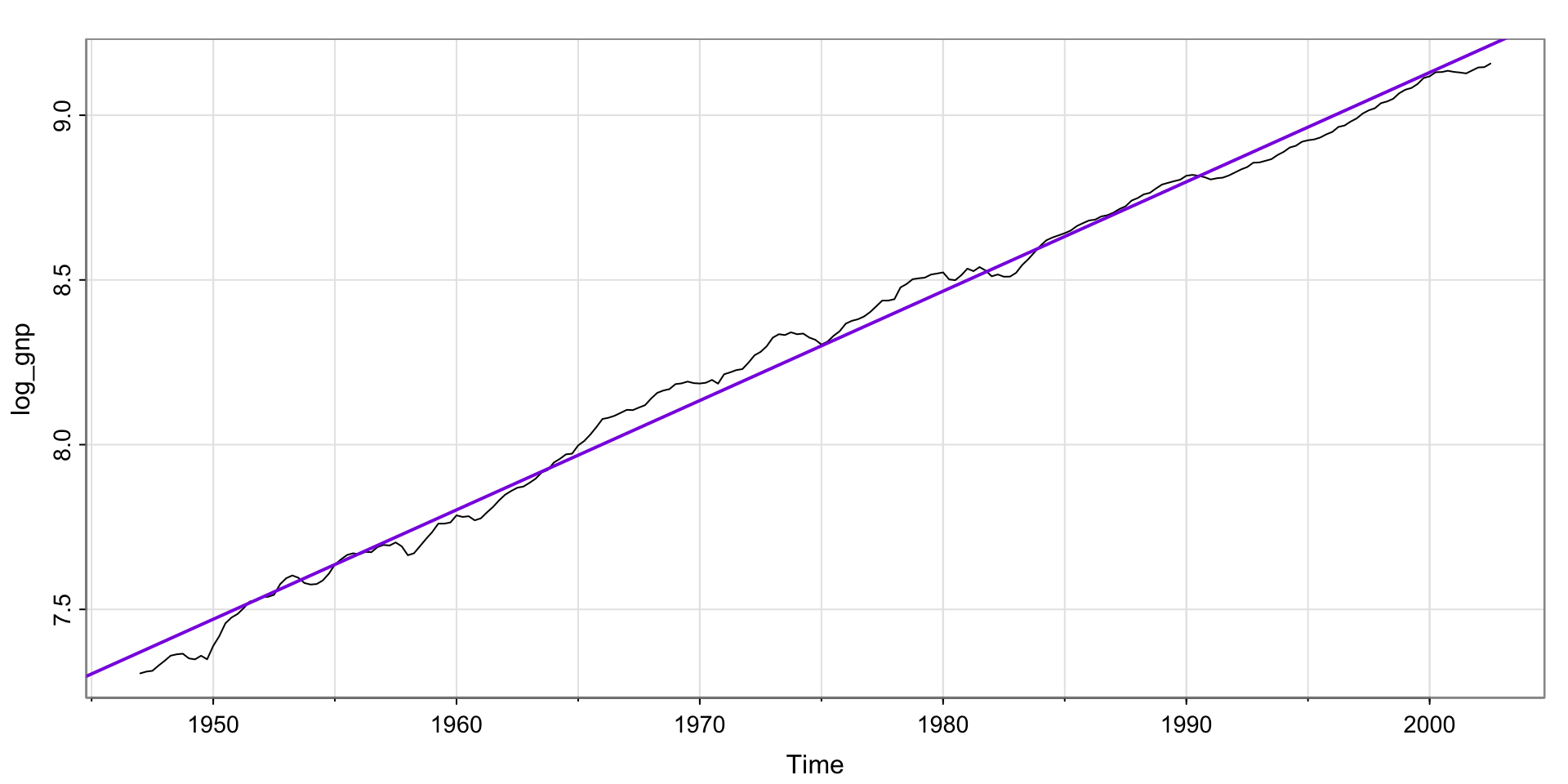

Try taking the log?

Much better! But, still not stationary.

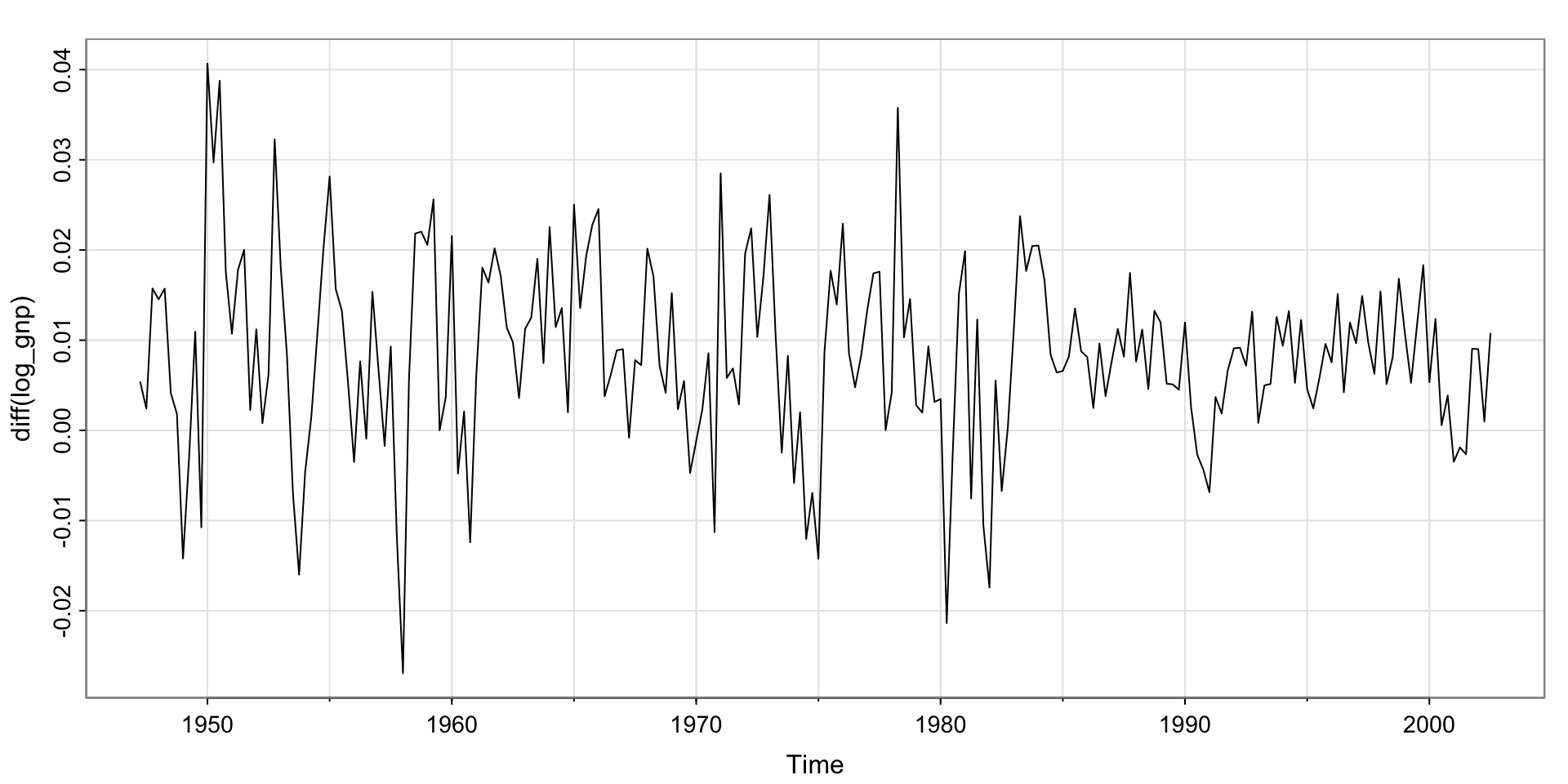

Try differencing?

Is this stationary? No? Yes? Maybe there’s a bit of a trend?

Recall the ARIMA modeling workflow

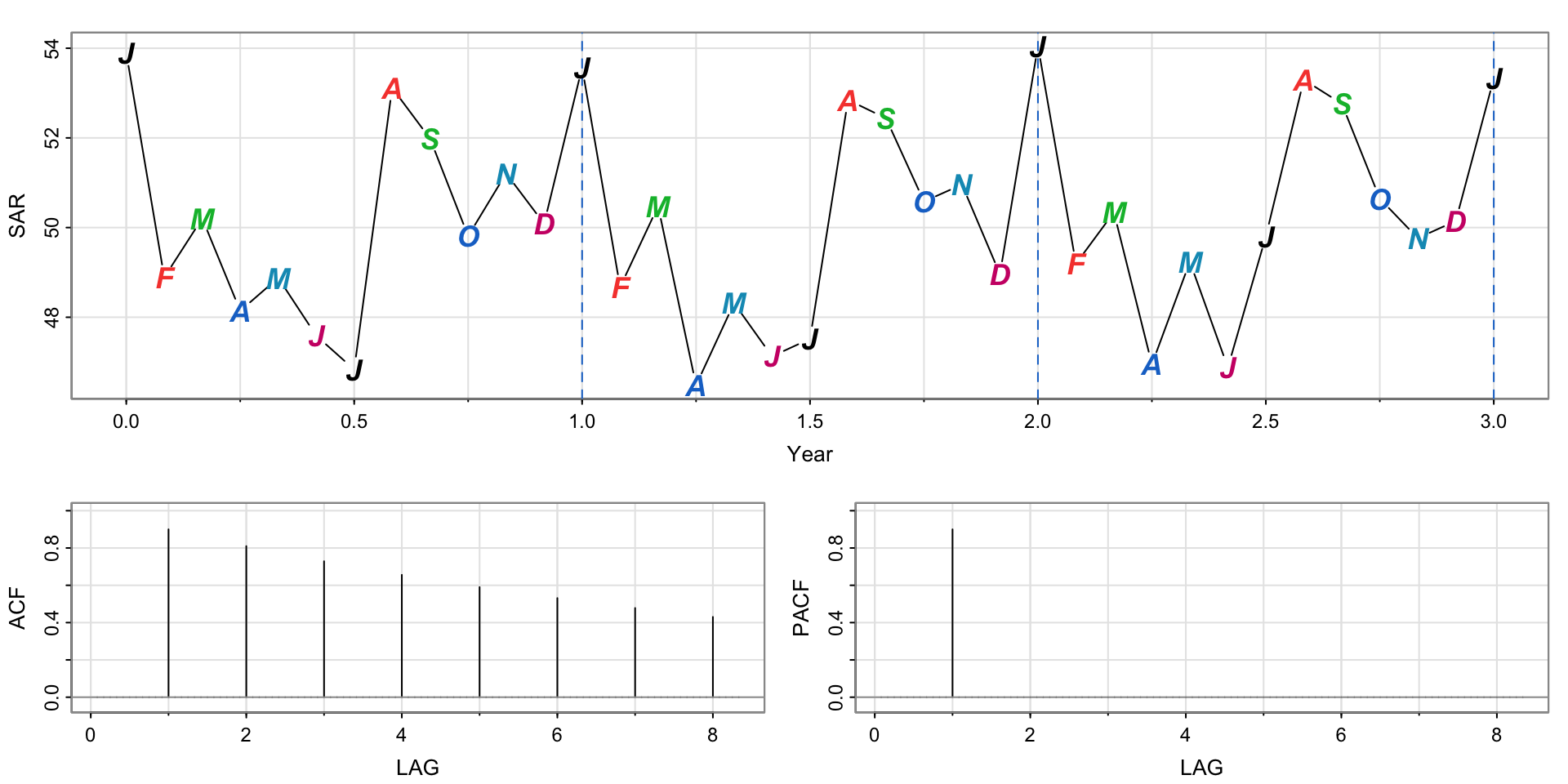

Activity 1 Solutions (manual)

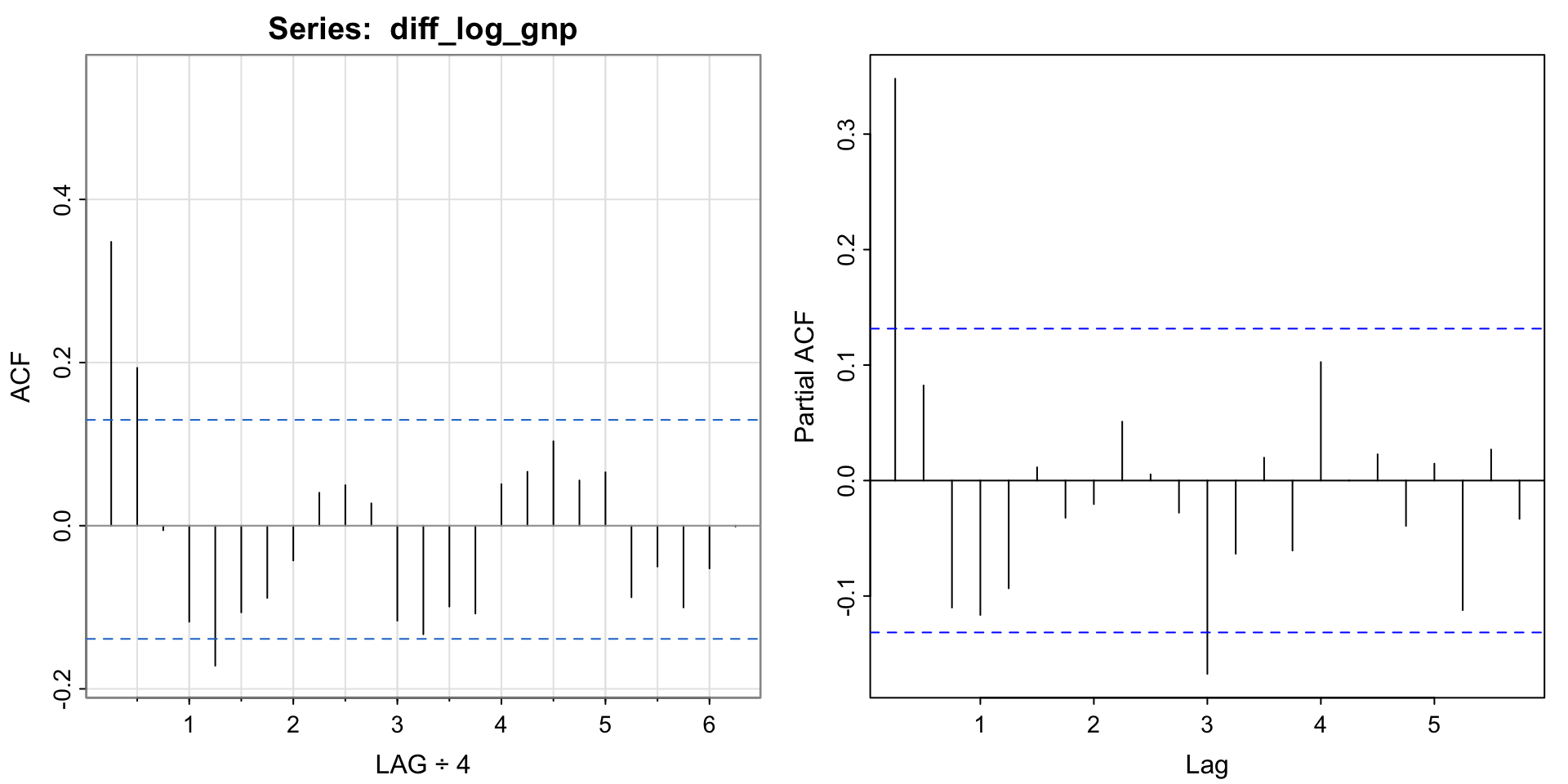

Manual: look at ACF and PACF. The ACF maybe cuts at lag 2 and the PACF appears to tail off. So maybe MA(2)?

Code

[1] 0.35 0.19 -0.01 -0.12 -0.17 -0.11 -0.09 -0.04 0.04 0.05 0.03 -0.12

[13] -0.13 -0.10 -0.11 0.05 0.07 0.10 0.06 0.07 -0.09 -0.05 -0.10 -0.05

[25] 0.00

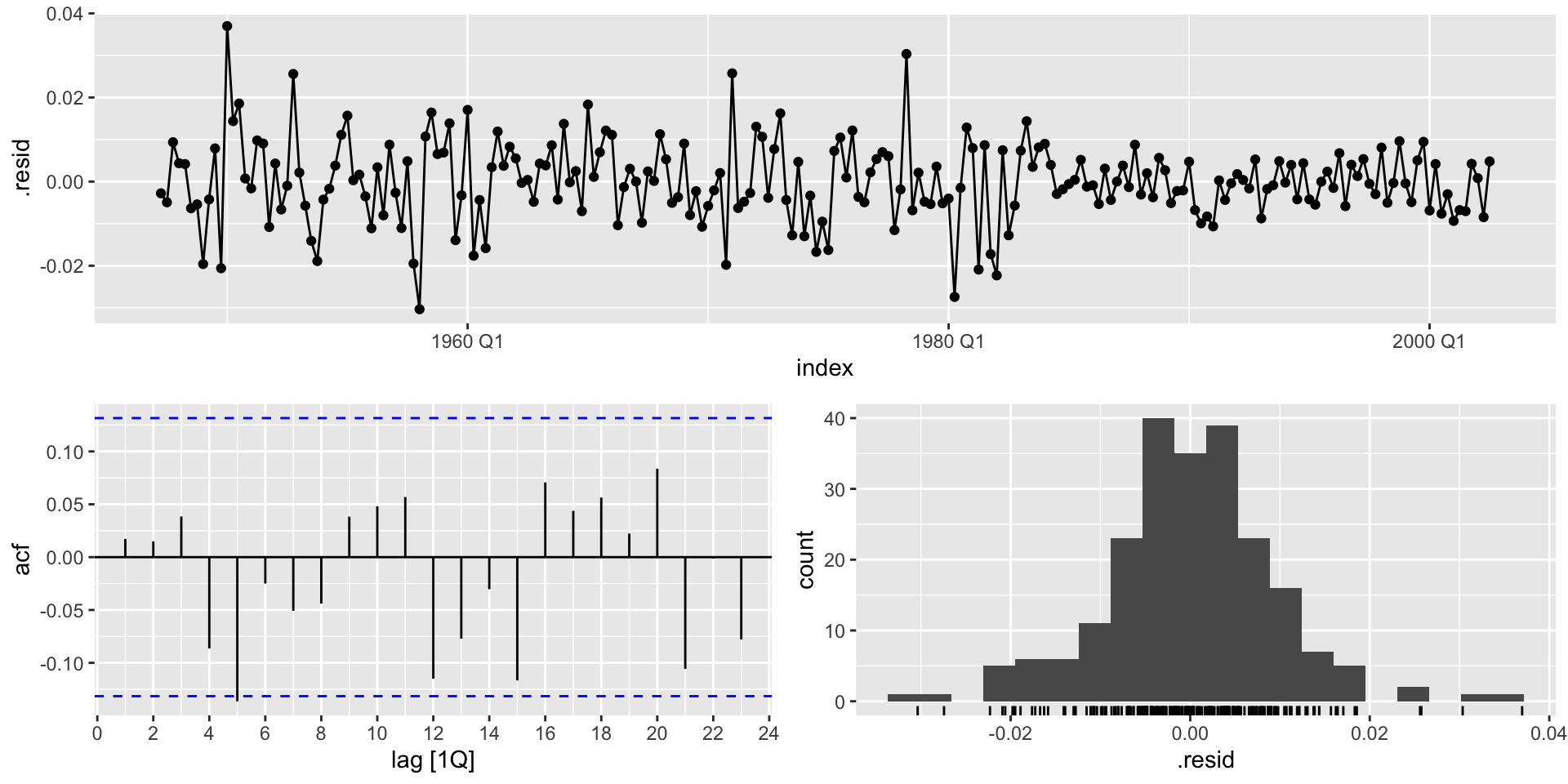

Activity 1 Solutions

The residuals look like white noise

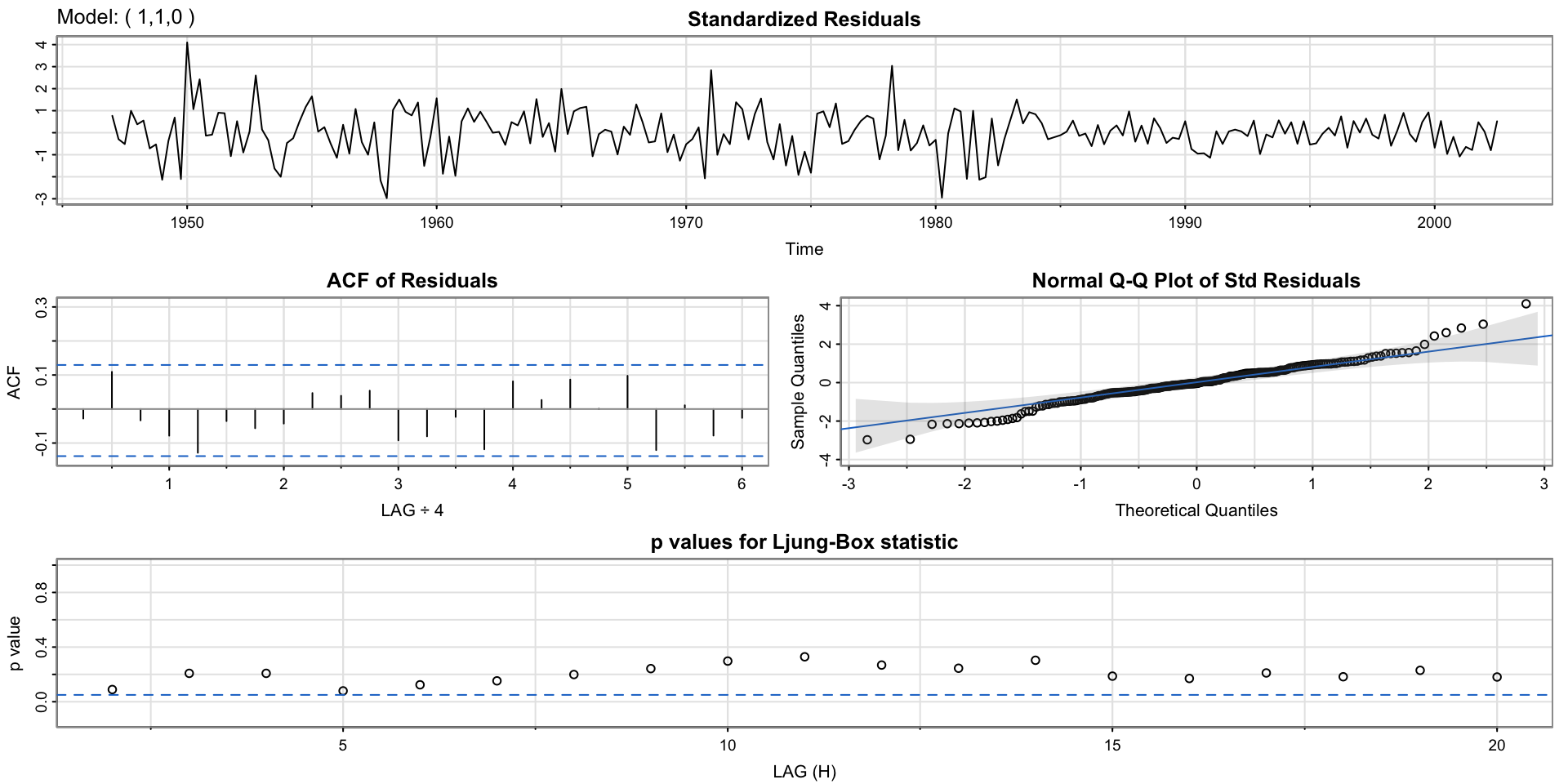

Using the sarima function for diagnostics

initial value -4.589567

iter 2 value -4.654150

iter 3 value -4.654150

iter 4 value -4.654151

iter 4 value -4.654151

iter 4 value -4.654151

final value -4.654151

converged

initial value -4.655919

iter 2 value -4.655921

iter 3 value -4.655921

iter 4 value -4.655922

iter 5 value -4.655922

iter 5 value -4.655922

iter 5 value -4.655922

final value -4.655922

converged

<><><><><><><><><><><><><><>

Coefficients:

Estimate SE t.value p.value

ar1 0.3467 0.0627 5.5255 0

constant 0.0083 0.0010 8.5398 0

sigma^2 estimated as 9.029576e-05 on 220 degrees of freedom

AIC = -6.446939 AICc = -6.446692 BIC = -6.400957

Simulating a pure seasonal AR(1) process

Notice the peaks every January– the seasonal period here is 12 (or 1 if we divide by 12).

The same “tailing off”/“cutting off” behavior is the same, but we look for seasonal spikes

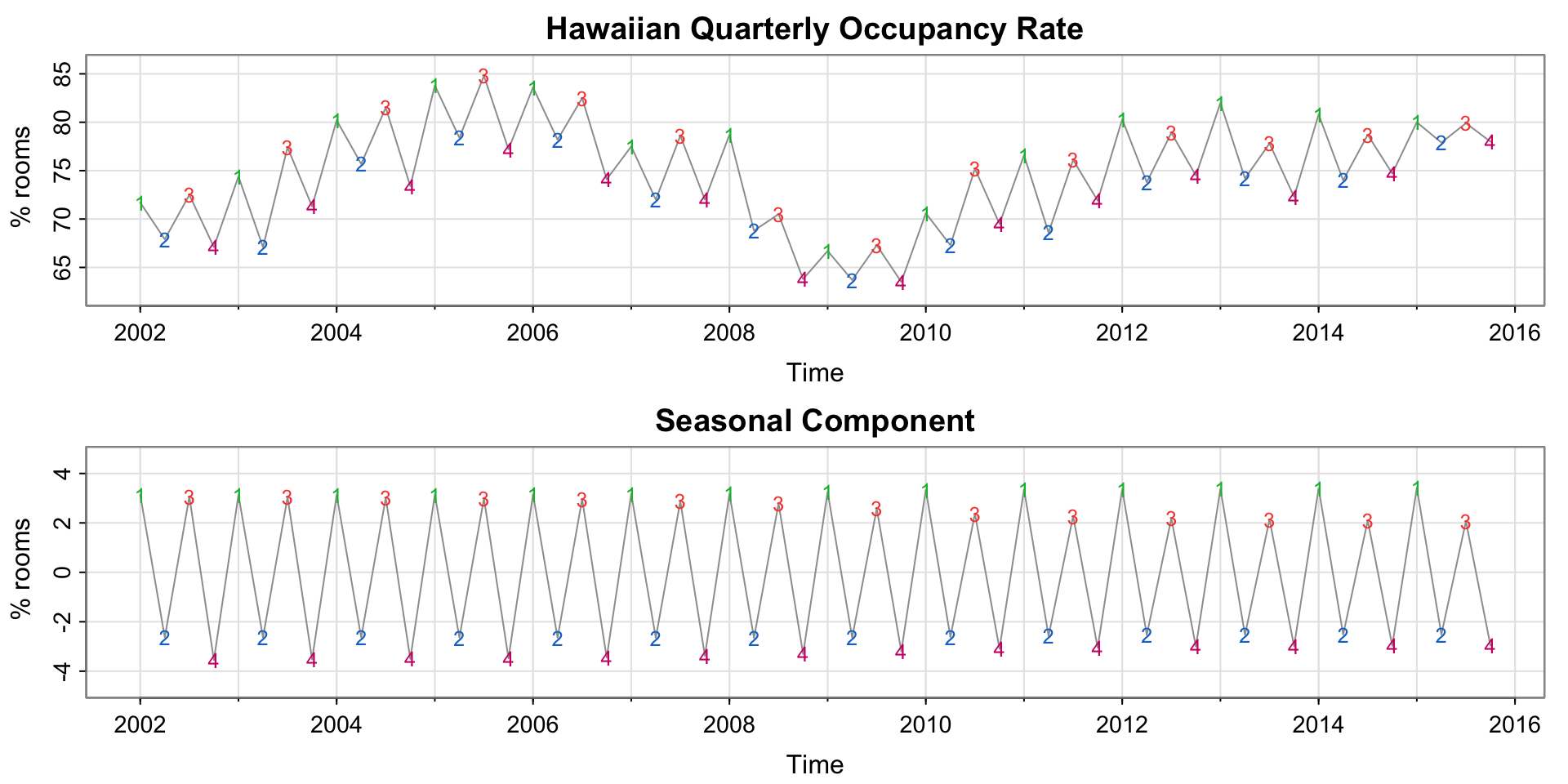

Hawaiian Quarterly Occupancy

The two plots show the time series, and the extracted seasonal component.

Hawaiian Quarterly Occupancy

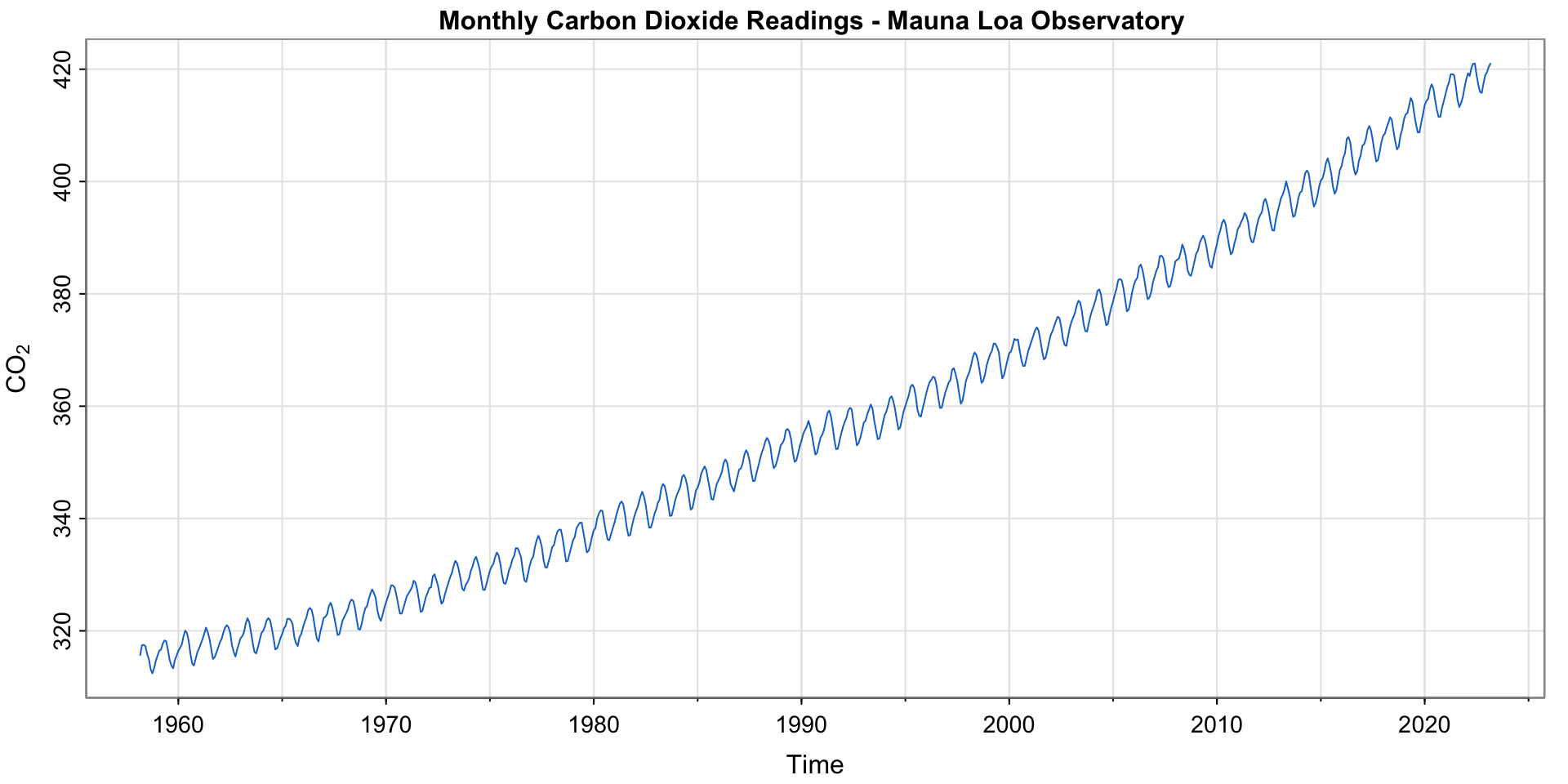

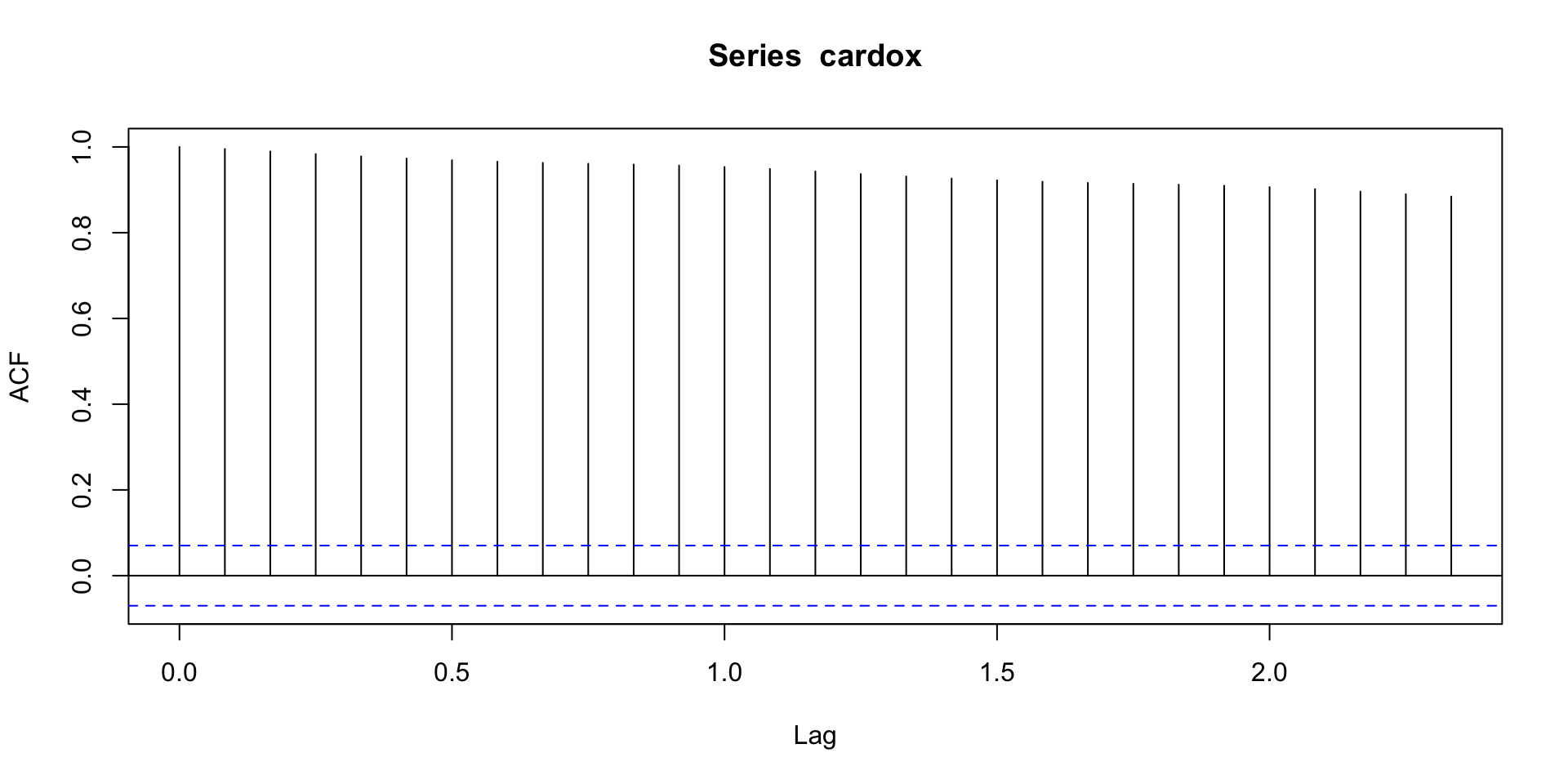

Carbon Dioxide Readings

Monthly \(CO_2\) readings at Mauna Loa Observatory

Do we see a seasonal pattern?

What’s the acf?

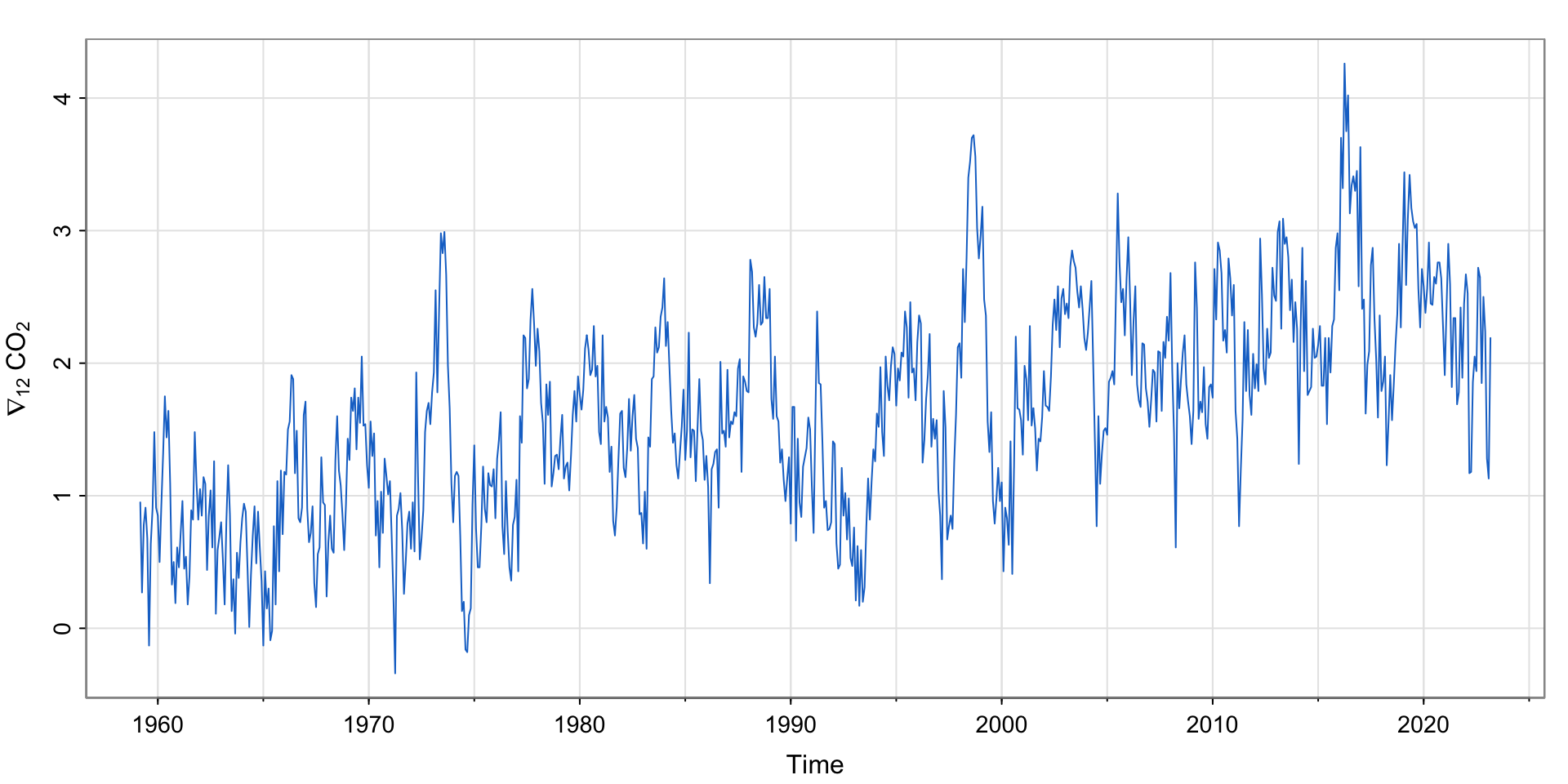

Let’s try a seasonal difference!

Check the acf

Still a trend..difference again?

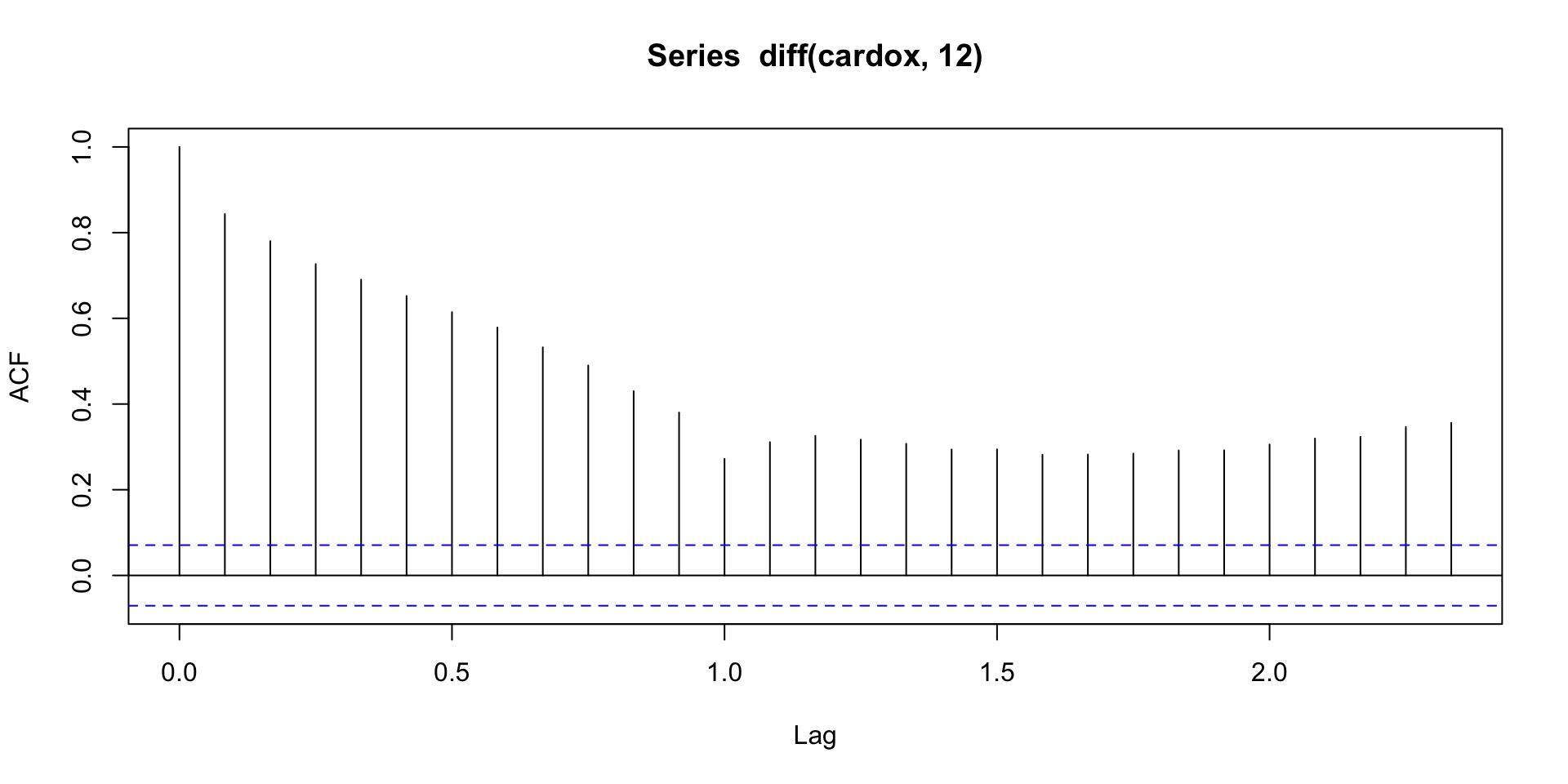

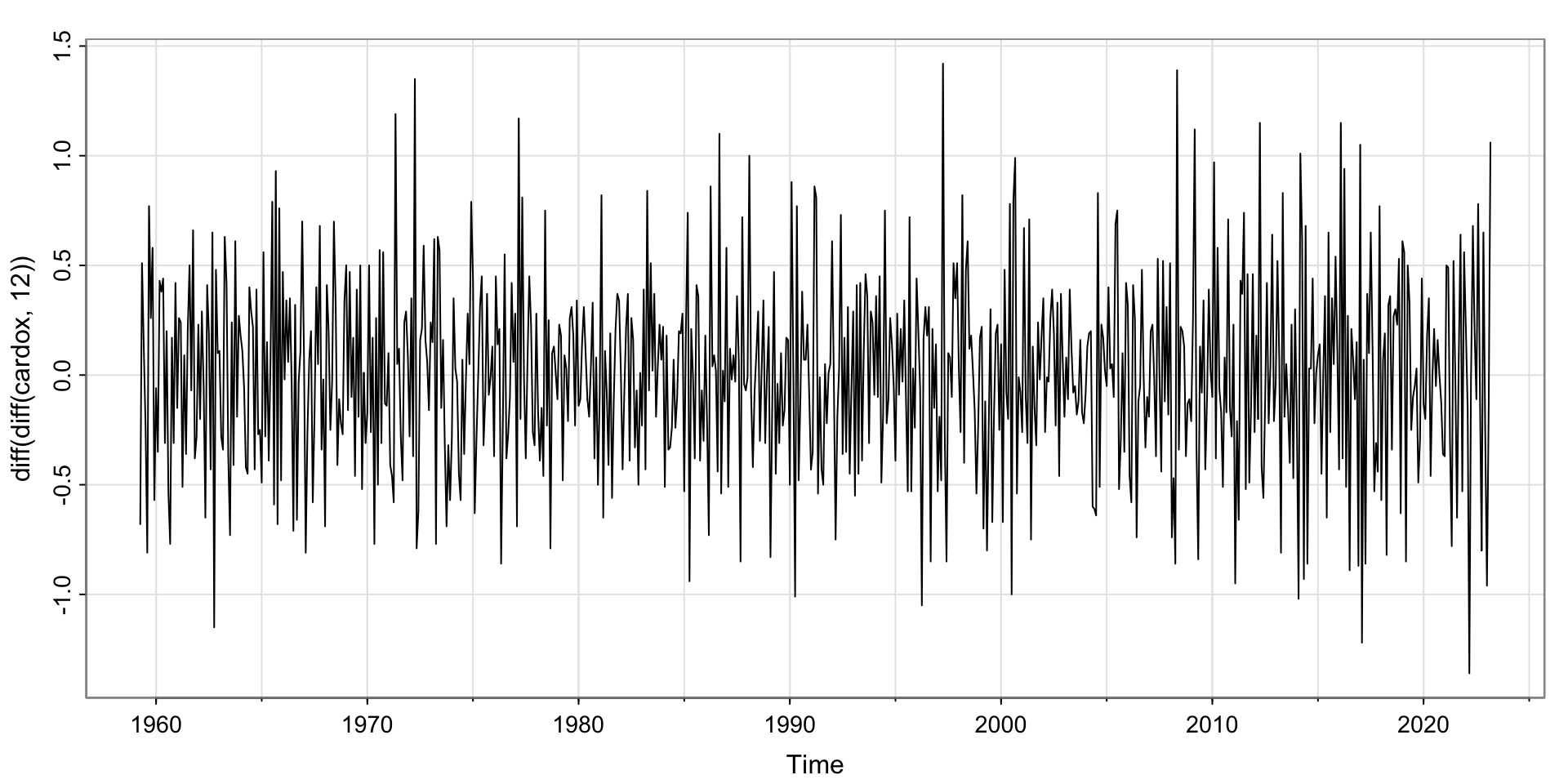

Difference and Seasonal Difference

Looks pretty stationary!

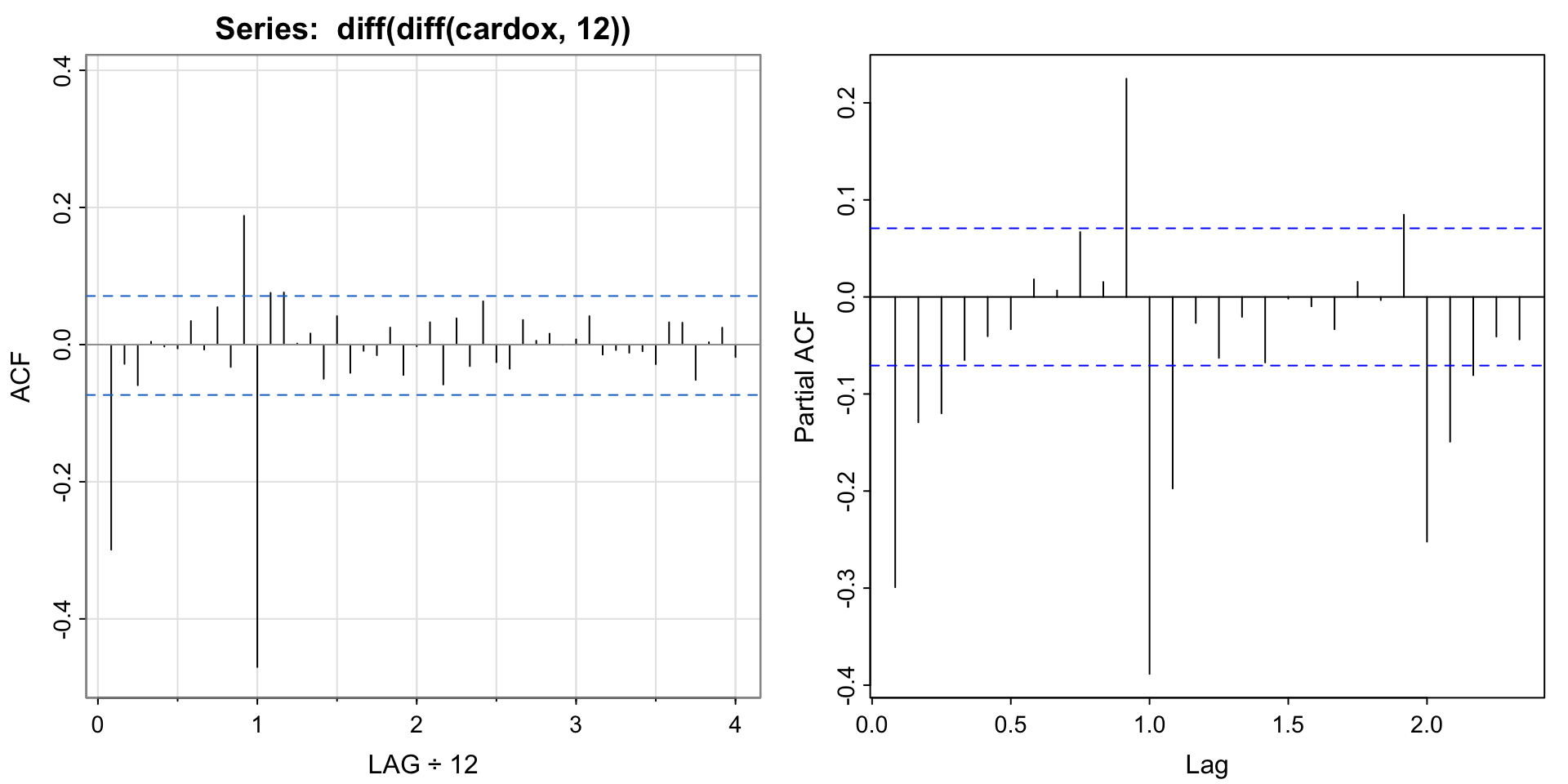

\(p,q\) and \(P,Q\) for Carbon Dioxide

Seasonal: ACF appears to cut off at lag 1 (12 months), but tails of at lags 1, 2, 3, 4– implies a seasonal moving average, so \(Q=1, P= 0\).

Non-seasonal: Appears to cut off at lag 1 (1/12) and PACF tails off. Looks like a MA(1), so \(q = 1, p = 0\).

[1] -0.30 -0.03 -0.06 0.00 0.00 -0.01 0.03 -0.01 0.05 -0.03 0.19 -0.47

[13] 0.08 0.08 0.00 0.02 -0.05 0.04 -0.04 -0.01 -0.02 0.02 -0.04 0.00

[25] 0.03 -0.06 0.04 -0.03 0.06 -0.03 -0.04 0.04 0.01 0.02 0.00 0.01

[37] 0.04 -0.01 -0.01 -0.01 -0.01 -0.03 0.03 0.03 -0.05 0.00 0.02 -0.02

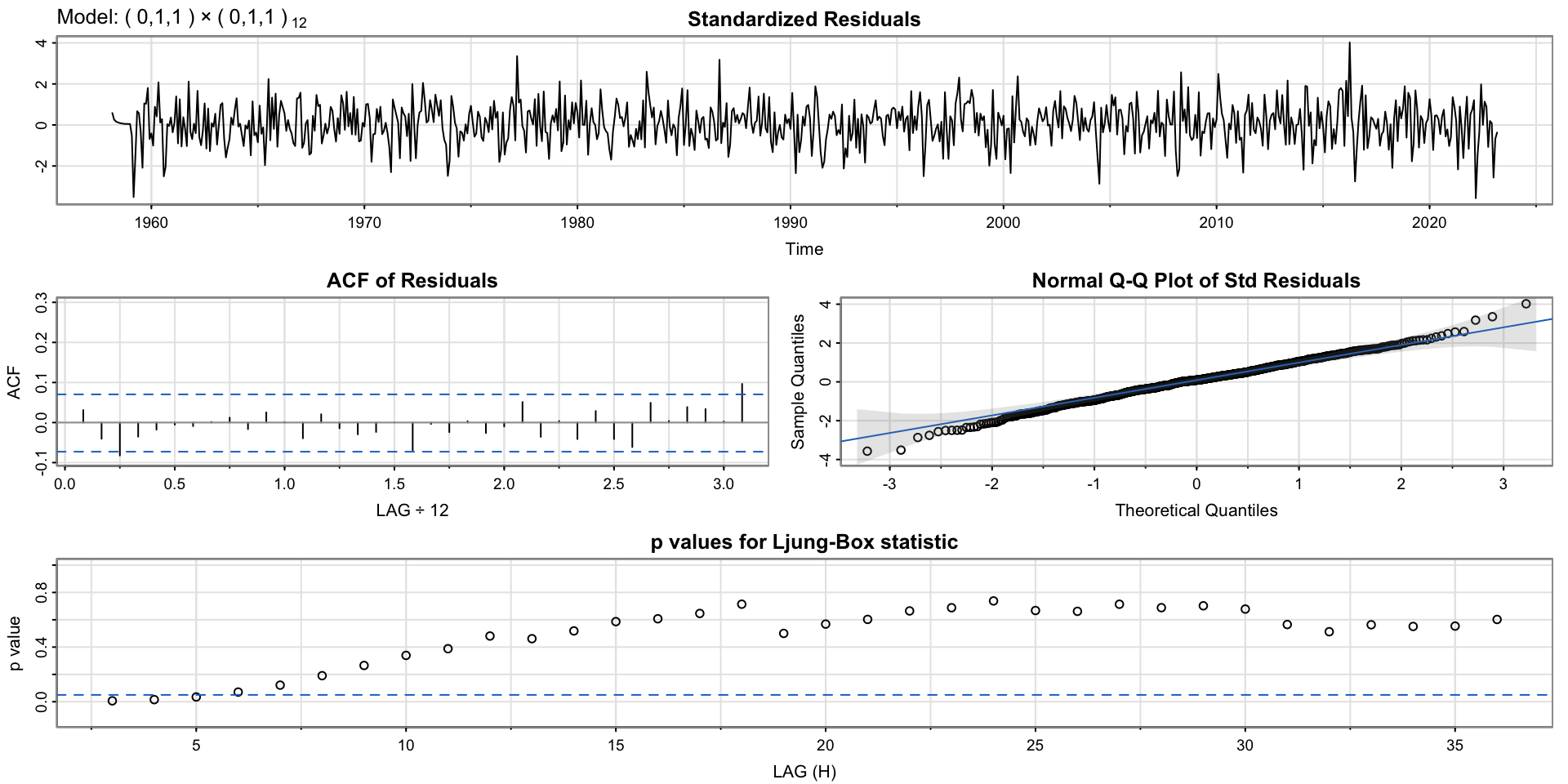

Fit \(ARIMA(0,1,1)\times(0,1,1)_{12}\)

initial value -0.826338

iter 2 value -1.059073

iter 3 value -1.093845

iter 4 value -1.116555

iter 5 value -1.124382

iter 6 value -1.126345

iter 7 value -1.127354

iter 8 value -1.127953

iter 9 value -1.127984

iter 10 value -1.127985

iter 10 value -1.127985

iter 10 value -1.127985

final value -1.127985

converged

initial value -1.144615

iter 2 value -1.148048

iter 3 value -1.148645

iter 4 value -1.149895

iter 5 value -1.150013

iter 6 value -1.150021

iter 7 value -1.150021

iter 7 value -1.150021

iter 7 value -1.150021

final value -1.150021

converged

<><><><><><><><><><><><><><>

Coefficients:

Estimate SE t.value p.value

ma1 -0.3869 0.0377 -10.2624 0

sma1 -0.8655 0.0183 -47.2846 0

sigma^2 estimated as 0.0980908 on 766 degrees of freedom

AIC = 0.5456475 AICc = 0.545668 BIC = 0.5637873

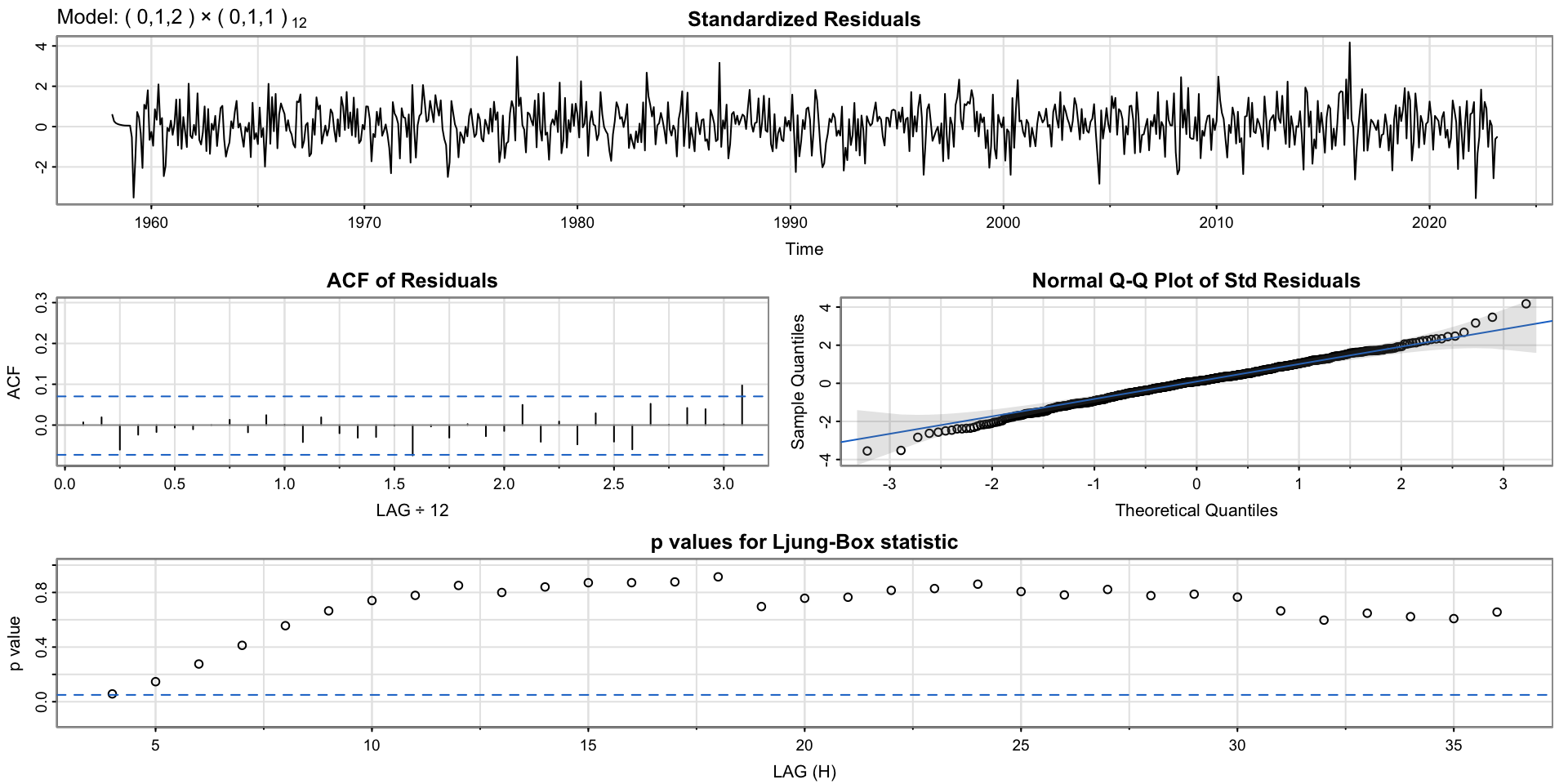

Increase order of MA

initial value -0.826338

iter 2 value -1.061232

iter 3 value -1.098226

iter 4 value -1.120391

iter 5 value -1.127720

iter 6 value -1.129516

iter 7 value -1.130690

iter 8 value -1.130938

iter 9 value -1.130955

iter 10 value -1.130959

iter 11 value -1.130959

iter 12 value -1.130959

iter 12 value -1.130959

iter 12 value -1.130959

final value -1.130959

converged

initial value -1.147318

iter 2 value -1.150711

iter 3 value -1.151405

iter 4 value -1.152442

iter 5 value -1.152564

iter 6 value -1.152573

iter 7 value -1.152574

iter 7 value -1.152574

iter 7 value -1.152574

final value -1.152574

converged

<><><><><><><><><><><><><><>

Coefficients:

Estimate SE t.value p.value

ma1 -0.3678 0.0359 -10.2365 0.0000

ma2 -0.0704 0.0354 -1.9911 0.0468

sma1 -0.8651 0.0182 -47.4548 0.0000

sigma^2 estimated as 0.09759346 on 765 degrees of freedom

AIC = 0.5431467 AICc = 0.5431876 BIC = 0.5673331

initial value -0.827261

iter 2 value -1.034332

iter 3 value -1.066295

iter 4 value -1.094823

iter 5 value -1.108013

iter 6 value -1.115246

iter 7 value -1.116173

iter 8 value -1.120248

iter 9 value -1.120892

iter 10 value -1.121657

iter 11 value -1.122186

iter 12 value -1.124590

iter 13 value -1.125269

iter 14 value -1.125654

iter 15 value -1.125685

iter 16 value -1.125685

iter 17 value -1.125687

iter 18 value -1.125689

iter 19 value -1.125689

iter 20 value -1.125689

iter 20 value -1.125689

iter 20 value -1.125689

final value -1.125689

converged

initial value -1.146682

iter 2 value -1.150731

iter 3 value -1.152123

iter 4 value -1.152815

iter 5 value -1.153157

iter 6 value -1.153220

iter 7 value -1.153266

iter 8 value -1.153337

iter 9 value -1.153352

iter 10 value -1.153359

iter 11 value -1.153384

iter 12 value -1.153388

iter 13 value -1.153390

iter 14 value -1.153390

iter 14 value -1.153390

iter 14 value -1.153390

final value -1.153390

converged

<><><><><><><><><><><><><><>

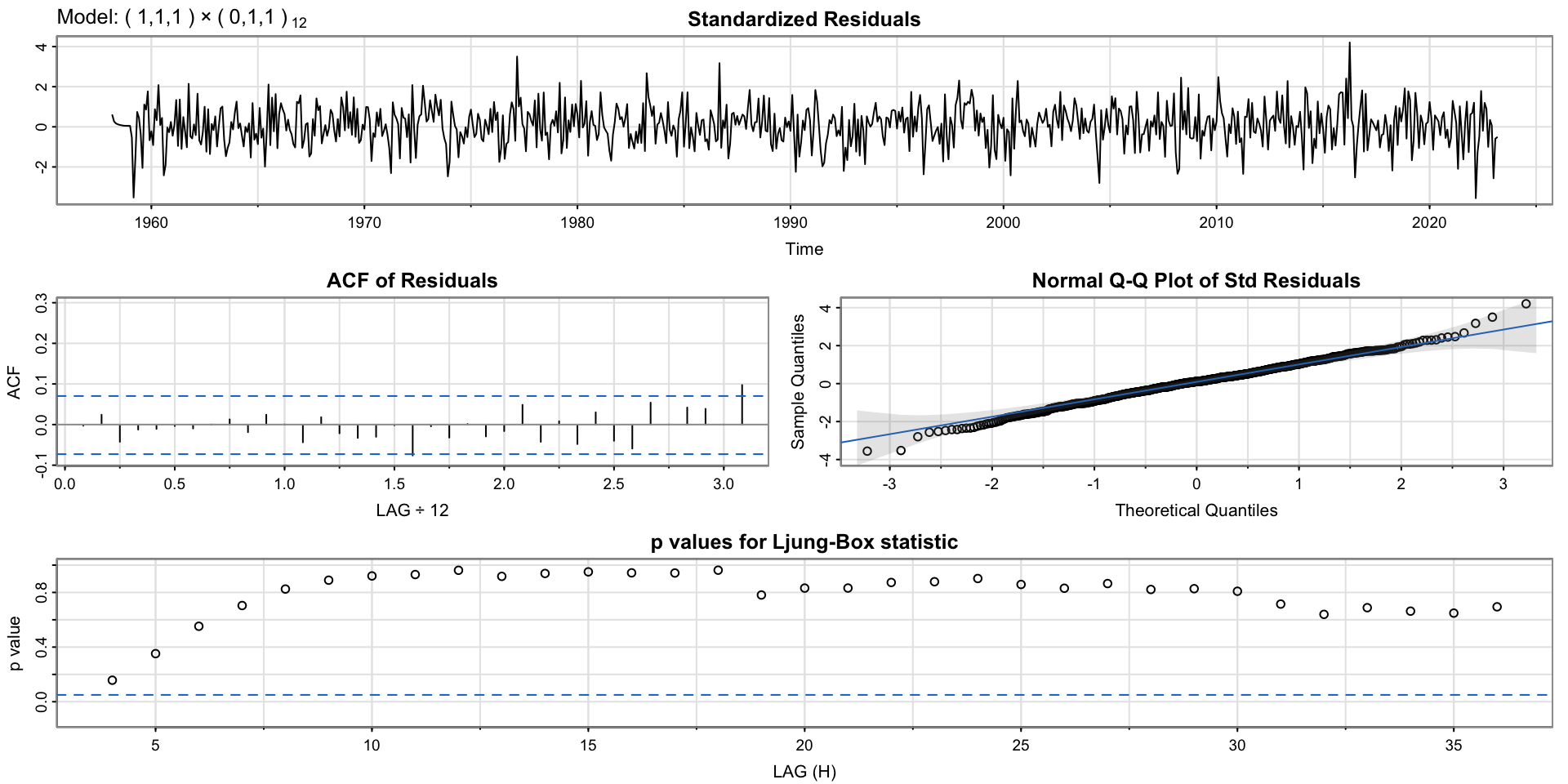

Coefficients:

Estimate SE t.value p.value

ar1 0.2203 0.0894 2.4660 0.0139

ma1 -0.5797 0.0753 -7.7029 0.0000

sma1 -0.8656 0.0182 -47.5947 0.0000

sigma^2 estimated as 0.09742764 on 765 degrees of freedom

AIC = 0.541514 AICc = 0.5415549 BIC = 0.5657004

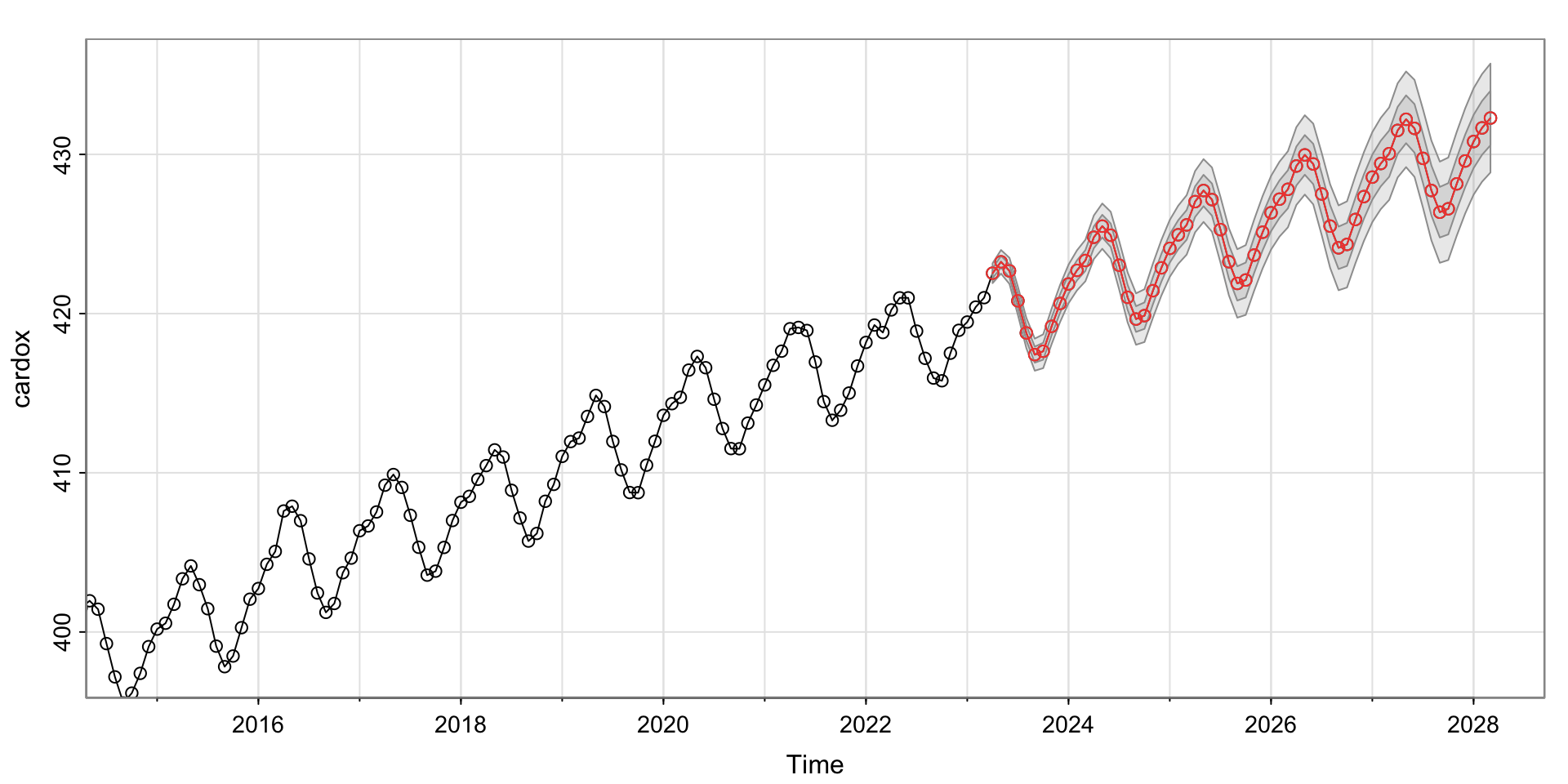

Forecasting

Looks like we predict the \(CO_2\) to continue to increase…

$pred

Jan Feb Mar Apr May Jun Jul Aug

2023 422.5365 423.2516 422.6841 420.8017 418.7844

2024 421.8604 422.7144 423.3343 424.7951 425.4936 424.9223 423.0392 421.0216

2025 424.0976 424.9517 425.5715 427.0323 427.7308 427.1595 425.2764 423.2588

2026 426.3348 427.1889 427.8088 429.2695 429.9680 429.3968 427.5136 425.4961

2027 428.5720 429.4261 430.0460 431.5067 432.2052 431.6340 429.7509 427.7333

2028 430.8092 431.6633 432.2832

Sep Oct Nov Dec

2023 417.4195 417.6341 419.1994 420.6362

2024 419.6567 419.8713 421.4367 422.8734

2025 421.8940 422.1085 423.6739 425.1106

2026 424.1312 424.3458 425.9111 427.3479

2027 426.3684 426.5830 428.1483 429.5851

2028

$se

Jan Feb Mar Apr May Jun Jul

2023 0.3121340 0.3706892 0.4100237 0.4437896

2024 0.6057658 0.6286983 0.6508233 0.6839230 0.7112115 0.7366194 0.7609956

2025 0.8931404 0.9133056 0.9330350 0.9616380 0.9859772 1.0090191 1.0313946

2026 1.1563743 1.1759118 1.1951299 1.2221148 1.2455209 1.2678703 1.2896982

2027 1.4134077 1.4329864 1.4523012 1.4786701 1.5018653 1.5241385 1.5459682

2028 1.6707850 1.6906907 1.7103647

Aug Sep Oct Nov Dec

2023 0.4747345 0.5036938 0.5310578 0.5570754 0.5819301

2024 0.7845756 0.8074590 0.8297096 0.8513785 0.8725094

2025 1.0532622 1.0746779 1.0956735 1.1162740 1.1365011

2026 1.3111337 1.3322181 1.3529726 1.3734132 1.3935539

2027 1.5674673 1.5886697 1.6095915 1.6302447 1.6506393

2028 $pred

Jan Feb Mar Apr May Jun Jul Aug

2023 422.5365 423.2516 422.6841 420.8017 418.7844

2024 421.8604 422.7144 423.3343 424.7951 425.4936 424.9223 423.0392 421.0216

2025 424.0976 424.9517 425.5715 427.0323 427.7308 427.1595 425.2764 423.2588

2026 426.3348 427.1889 427.8088 429.2695 429.9680 429.3968 427.5136 425.4961

2027 428.5720 429.4261 430.0460 431.5067 432.2052 431.6340 429.7509 427.7333

2028 430.8092 431.6633 432.2832

Sep Oct Nov Dec

2023 417.4195 417.6341 419.1994 420.6362

2024 419.6567 419.8713 421.4367 422.8734

2025 421.8940 422.1085 423.6739 425.1106

2026 424.1312 424.3458 425.9111 427.3479

2027 426.3684 426.5830 428.1483 429.5851

2028

$se

Jan Feb Mar Apr May Jun Jul

2023 0.3121340 0.3706892 0.4100237 0.4437896

2024 0.6057658 0.6286983 0.6508233 0.6839230 0.7112115 0.7366194 0.7609956

2025 0.8931404 0.9133056 0.9330350 0.9616380 0.9859772 1.0090191 1.0313946

2026 1.1563743 1.1759118 1.1951299 1.2221148 1.2455209 1.2678703 1.2896982

2027 1.4134077 1.4329864 1.4523012 1.4786701 1.5018653 1.5241385 1.5459682

2028 1.6707850 1.6906907 1.7103647

Aug Sep Oct Nov Dec

2023 0.4747345 0.5036938 0.5310578 0.5570754 0.5819301

2024 0.7845756 0.8074590 0.8297096 0.8513785 0.8725094

2025 1.0532622 1.0746779 1.0956735 1.1162740 1.1365011

2026 1.3111337 1.3322181 1.3529726 1.3734132 1.3935539

2027 1.5674673 1.5886697 1.6095915 1.6302447 1.6506393

2028